I don’t pay much attention to quarterly stock market changes. I don’t spend time trying to read tea leaves either. However, when the market goes down 10% or more from its peak, it spurs me into action. Why? As I detailed in this blog entry, I have a cash-as-dry-powder strategy. Whenever the stock market goes down by 10% or more, I deploy some of my dry powder.

I don’t pay much attention to quarterly stock market changes. I don’t spend time trying to read tea leaves either. However, when the market goes down 10% or more from its peak, it spurs me into action. Why? As I detailed in this blog entry, I have a cash-as-dry-powder strategy. Whenever the stock market goes down by 10% or more, I deploy some of my dry powder.

It turns out that 1Q 2018 was such a quarter after a long while. Stocks went up in January and then dropped 11% from their peak in early February. They mostly treaded sideways for the rest of the quarter – bouncing around its lows.

Following my dry powder rulebook, I invested 10% of cash into stocks when the market went down this last quarter. I make no attempt to predict where the market might go next. If stocks go down further from here, I will have another tranche of cash ready to be deployed. If market recovers from here and regain its previous high, I will then have the opportunity to replenish the dry powder by taking profits elsewhere.

As you can see from my portfolio, I have positions in stock index funds. I usually sell a portion of those investments to rebuild my dry powder whenever the market recovers. Of course how long the market takes to recover is entirely unknown to me (for that matter, to anyone else too). But I am patient with my investing strategy.

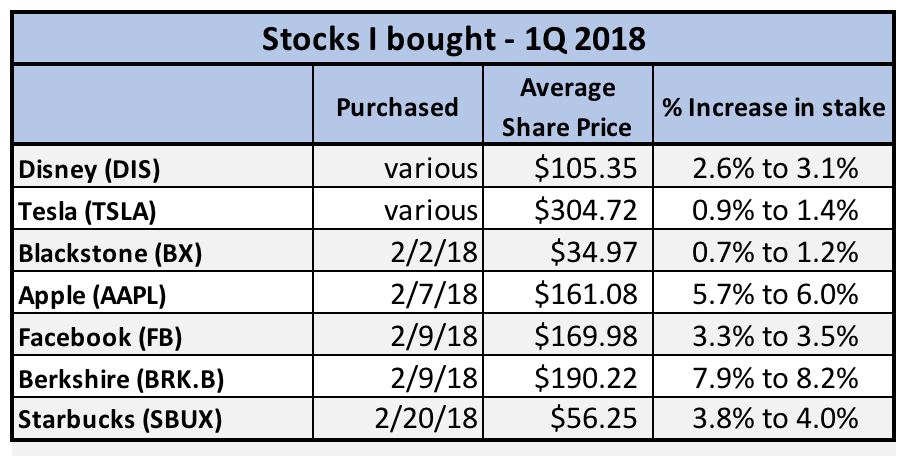

Stock purchases: I didn’t sell any positions in 1Q. All my stock purchases were additive to my existing positions. None of them were new to me. Generally, I buy an incremental position whenever I believe that the valuation is reasonable, my investment thesis is still intact, and I have money available to invest. You will see these recurring themes in my stock updates below.

Disney (DIS): I bought Disney twice in the quarter. Once at $110 and then later when its price dropped to about $100.

Disney’s parks and movies businesses are doing very well – thanks to good economy and highly successful recent movie releases. Where it’s been hurting last few quarters is in media networks – mainly because of ESPN and on-going concerns about cord-cutting. To me though, its recent troubles are temporary.

There is a paradigm shift going on in the cable TV business. Consumers want more choices and Internet streaming is allowing them to drop expensive cable subscriptions. They don’t want to pay for content they don’t consume. If I don’t watch live sports, why should I pay for it? ESPN, given its wide licensing agreements with all major sports leagues, gets a substantial portion of monthly cable fees from distributors. And this licensing (or affiliate) revenue is what concerns the market. Would it go away eventually – or drop significantly enough such that the company’s multi-year licensing deals with sports leagues become unprofitable? This, in a nutshell, is investors’ concern.

From my perspective though, the odds are quite good that Disney will maintain its sports viewership – in one form or another. It’s already moving towards direct to consumer online streaming subscriptions. ESPN has the best brand recognition out there. Its recently launched ESPN+ streaming app is a first step towards a la carte sports subscription. It plans to do the same with a Disney themed streaming service next year. It acquired streaming technology recently from BAMtech. It also owns a stake in the Hulu service.

At the same time, Disney is also bolstering its content ownership by acquiring Fox media assets – TV, movies and sports related. It’s a fairly large deal – that will result in Disney issuing 25% new shares for Fox’s owners. If they can get regulatory approvals (could take up to 18 months), it will be a good move to consolidate more high-quality media assets. Disney CEO Bob Iger’s prior acquisition record has been exceptionally good – with names like Pixar, Marvel Studios, Lucas Films. He’s been at the helm since 2005 and expected to continue for at least another two years.

When I first bought shares in January, its trailing P/E ratio was 20 which was below market average and looked reasonable to me. At the time, I expected about 10% return on my investment (CAGR) with 7% earnings growth over next 10 years and leveling off to 3% afterward – assuming no increase in the earnings multiple.

The second time I bought shares in March, its trailing P/E had dropped to 14 thanks to 22% increase in 1Q EPS. This was clearly an even better value than before.

![]() Berkshire Hathaway (BRK.B): What can I say about Berkshire that hasn’t already been said? It’s a permanent feature in my portfolio. It’s my second largest position so far – behind Amazon. I add to my position whenever the stock drops or its valuation becomes compelling. Last time I bought, it was in May 2017 when its stock price was trading at 1.4 times the book value. When I bought again in February this year, the stock was down about 13% from its 52-week high and it was trading at 1.5 times book value. Not very cheap but reasonable given where the overall market is. For comparison, Berkshire’s five-year average is 1.42 times book value.

Berkshire Hathaway (BRK.B): What can I say about Berkshire that hasn’t already been said? It’s a permanent feature in my portfolio. It’s my second largest position so far – behind Amazon. I add to my position whenever the stock drops or its valuation becomes compelling. Last time I bought, it was in May 2017 when its stock price was trading at 1.4 times the book value. When I bought again in February this year, the stock was down about 13% from its 52-week high and it was trading at 1.5 times book value. Not very cheap but reasonable given where the overall market is. For comparison, Berkshire’s five-year average is 1.42 times book value.

Like most financial companies, book value is a good representation of Berkshire’s intrinsic value. I previously wrote about Berkshire’s book value in this post. The company’s share buyback plan also hinges upon its book value multiple. If the stock ever drops below 1.2 times the book value, it is authorized to start buying back its own shares. For all practical purposes, this means that Berkshire stock won’t ever drop below 1.2x its book value – given its large cash war chest.

These days, investors have two main concerns about Berkshire:

- What would happen when Buffet passes?

- Is the company too big to grow?

On the first question, it’s becoming pretty clear every passing year that Warren Buffet and the company board have already developed a succession plan. Buffett himself has said so on several occasions. But it appears that some investors will keep worrying until they see the details spelled out. That won’t happen until after Buffett and Munger relinquish control. From my viewpoint, this is perfectly fine. Buffet had plenty of time to think through the details. I expect his personnel decisions will be just as sound as his capital allocation decisions had been for the company.

On the latter concern, I believe that yes Berkshire won’t grow as fast as it did in its early years. You can also see this gradual slowing down effect in its book-value growth here in this chart. I expect it to remain a steady yet slow growth stock. Its performance will lag other higher growth businesses – especially in an economic expansion phase like today’s. But I expect it to remain steady-as-a-rock business when the next recession hits. Its many diverse business units will continue to generate good cash flow even during slow times. As I pointed out in my previous blog post, Berkshire’s book value has only ever dropped twice in previous 53 years.

Blackstone (BX): You can find my detailed investment thesis on Blackstone here in this post: Why I am buying Blackstone?

Blackstone (BX): You can find my detailed investment thesis on Blackstone here in this post: Why I am buying Blackstone?

I continue to build my stake in this company. 4Q results were excellent with Distributable Earnings (DE) growing over 80% (year over year). Total dividend distributed to unitholders in 2017 was $2.70 (per unit) – that yielded 7.40% at the time. As I outlined in the previous post, my expected return continues to be 12 to 14% annualized. AUM is growing nicely. They have new products in works that should drive new growth in AUM. Infrastructure and Insurance funds are already launched. There was some discussion on the earnings call about early stage growth equity products – but management wasn’t ready to give much details. Overall, Blackstone continues to do well, and I was happy to add to my stake this quarter.

To keep this post from getting too long, I will write about my remaining four purchases (Tesla, Facebook, Starbucks, and Apple) in a future article. [Here you go: Ed.] Among the four, Tesla stands out as a highly speculative investment while others are excellent proven businesses. Stay tuned for further thoughts on these.

[…] my last quarterly update, there haven’t been many changes in my portfolio. Stocks have been on the rise since April this […]