A lot of investor underperformance comes from them trying their utmost to avoid seeing losses. Emotionally, losses hurt twice as much as gains feel good. But there is no way to avoid seeing short-term losses in long-term investing. It’s inevitable for a long-term investor to see losses. Stocks are volatile in the short-run. They never rise (or fall) steadily. I wrote in a previous post that if stocks were not so volatile, investing would have been easy. Everyone would be investing in stocks and come out a winner. But that is not so.

What’s really important for long-term investors is to avoid permanent losses. Such as cashing out of the portfolio when it starts showing losses. Or buying shares of companies that do not have durable business models.

From time to time, even excellent seasoned investors see their portfolios go down in value:

Exhibit 1: Ken Fisher – the self-made billionaire founder of a very successful investment management firm, Fisher Investments. He’s also an insightful author. Fisher strives to predict large movements in the stock market. He’s been writing newspaper columns on his market predictions for last thirty years. How’s his record so far? Much better than most other prognosticators. And yet, he’s only right about two-third of the time according to the CXO Advisory Group. The group scored his forecasts from 2005 through 2012 along with 67 other experts. He managed to beat all but one other market expert for the period. You can see the results here.

I have been reading Fisher’s columns regularly for last fifteen years. I can tell you from first-hand experience that he totally missed the onset of the 2008 bear market.

Exhibit 2: Warren Buffett – the most successful investor in the history. He needs no introduction. Buffett’s entire net worth is concentrated in his company’s (Berkshire Hathaway) shares. He pointed out in his 2017 annual shareholder letter that Berkshire share prices have experienced four major declines in last 55 years. Each of those four dips had caused Buffett’s own net worth to drop by 40% to 60%.

Warren Buffett and Ken Fisher’s investing methods are very different, but they are both firm believers in long-term investing. Fisher strives to detect big market declines. Buffett doesn’t care—he doesn’t try to time but keeps good amount of dry powder cash ready when the market goes down.

If Buffett and Fisher can’t avoid short-term losses, what chances do I have as a lowly individual investor? Should I give up and not invest at all? Au contraire! I keep investing but I don’t count on predicting the market’s next big move. Fluctuations in my net worth are inevitable. Key is to stay the course I have chosen when the market hands me losses.

One mental construct that I use to keep myself prepared for short-term losses is to not be fixated to my portfolio’s current value. If you are the kind of investor who doesn’t look at your portfolio’s value often, you are doing it right. And I wish I were the same. But if you are like me, you might be checking your net worth periodically.

I use Quicken Premier software to track all my investments. Over the years, I have collected an assortment of retirement and brokerage accounts. And they are not all with the same custodian. Premier makes it real easy for me to collate all these accounts into one unified picture of my overall portfolio. The downside is that it also makes it easy for me to lookup my net worth with a quick glance.

Think in ranges: I prefer to think about my portfolio’s value (and indirectly, my own net worth) as a possible range—rather than one single number. It’s the low-end number in that range that’s really important as a mental hack. It helps me stay grounded. I am constantly reminded that my portfolio may be down to that low-end number some day in future. Would I be able to live with that? If it makes me lose sleep (actually, it doesn’t) I’d better do something about it today before it’s too late.

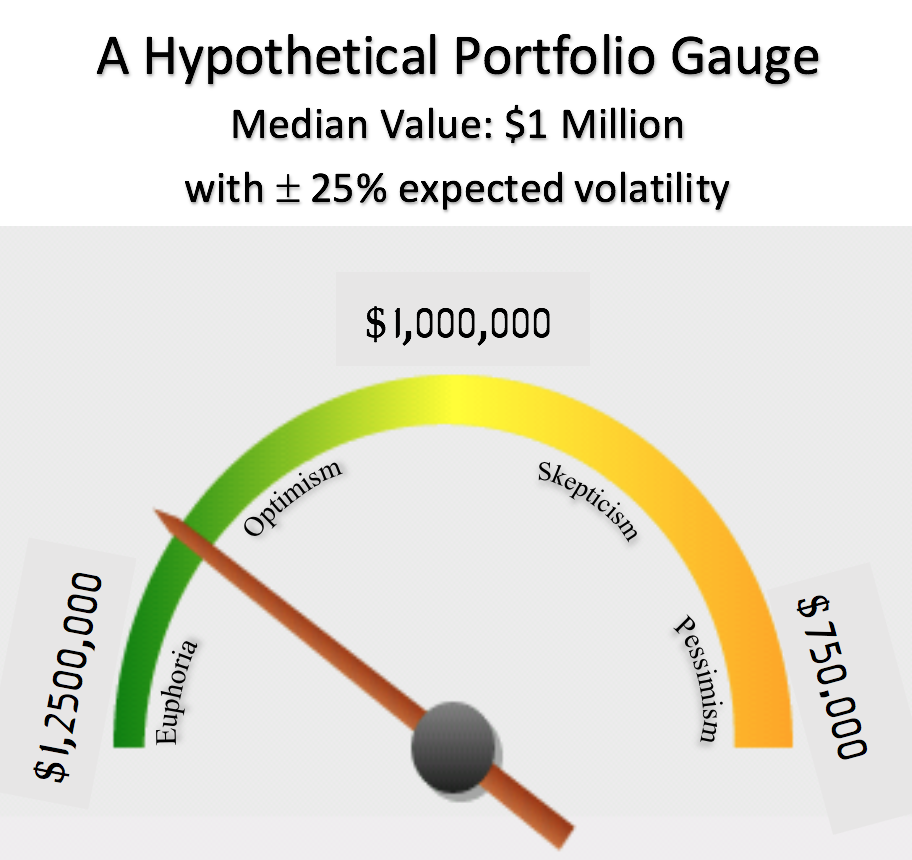

Just how big that range should be? It depends on the portfolio. In my case today, I consider an appropriate range to be plus–minus 25% above and below a median value.

Why just 25% variation even though the stock market is known to drop as much as 50% in severe bear markets? Partly because I have dry powder cash in my portfolio. And I own some alternative investments too.

Ten years ago, my portfolio was a lot more volatile. In fact, it did go down nearly 50% during the 2008 — 2009 Great Recession. But I also had significant number of employer stock options back then. Their value had quickly dropped to zero when the company shares went down. Today, this is not the case anymore. Back then, I would have been better off considering a wider range of volatility.

Picking a range to associate with the portfolio is not exact science. I believe 25% volatility around a median value reasonably reflects my portfolio today. But I could have just as well picked a different range – perhaps 30% or 40% up and down.

Here is one way to visualize a hypothetical one million-dollar portfolio whose value fluctuates by one-quarter … with a portfolio gauge:

Just like a real-life gauge, we don’t expect the needle of this meter to stay in one position for too long. It will swing—and so will my portfolio’s current value.

Of course, a portfolio’s value is also a function of time. If I keep making prudent moves (such as add more money, pick growing assets, avoid permanent losses), over time my portfolio would increase in value. Despite all the short-term turbulence in the stock market, we know from history that the US economy (and in general, of most developed countries) has gradually risen over time, and so has the valuation of public companies. I strive to achieve 10% annualized growth in my portfolio. If I successfully do that and reinvest all my profits, my portfolio should double in just about every seven years. Therefore, it is also rational for me to assess my portfolio’s median value every year or two—and nudge it higher as appropriate.

Looking at the gauge above, it also seems appropriate that today its needle is pointing to the left of the center. While I make no claims to when the market (and the US economy) would show a sustained decline, clearly my portfolio’s dollar value in today’s terms (just like in this hypothetical gauge) is on the high side of the range. I understand what that means, and I am prepared for the meter needle to swing right of the center someday.

Leave a Reply