In a word, no. Why do I say that? In this post, I will share my thoughts on dividends payers.

Across the universe of all publicly traded companies, I group them into three distinct buckets:

(1) Companies that pay generous dividend today (>4%). Though they tend to have low growth prospects e.g. public utilities (regulated local monopolies with stable but slow growth markets), or REITs/MLPs (required to distribute 90% of income as dividends which also results in frequent new-share issuances). From my own portfolio, it’s companies like Simon Property (SPG) and Kinder Morgan (KMI).

(2) Companies that are young and in high growth phase: they don’t pay dividends today and tend to reinvest all their cash-flow into further growth. But they could eventually start paying dividends once their businesses are sufficiently scaled. Companies like Tesla (TSLA) and Intuitive Surgical (ISRG) come to mind.

Some companies are not young anymore, but their addressable markets are still quite large. They also have good capital reinvestment opportunities and hence, not pay dividends either: Examples today would be Amazon (AMZN) and Berkshire (BRK.A/B)

(3) And then there are companies that have lowish dividends today but are expected to be growing them rapidly given their good growth prospects: I put Meta (META) and Alphabet (GOOG, GOOGL) from my portfolio in this bucket.

For companies that don’t pay dividends today, investors can manufacture their own dividends by selling a small fraction of shares every year. More on this a bit later.

Likewise, for companies that pay meager dividends today (1–2%), one could supplement this income by selling a fraction every year. Good businesses will grow their dividends every year so eventually one might not need to sell shares at all.

Why do some investors only focus on dividend-paying companies? Dividend payers are perceived to be less volatile. Perhaps so, but not always. Every year there are companies that cut dividends. About 2 out of 100 companies, in a typical year. When a company cuts its dividend, usually its stock falls significantly.

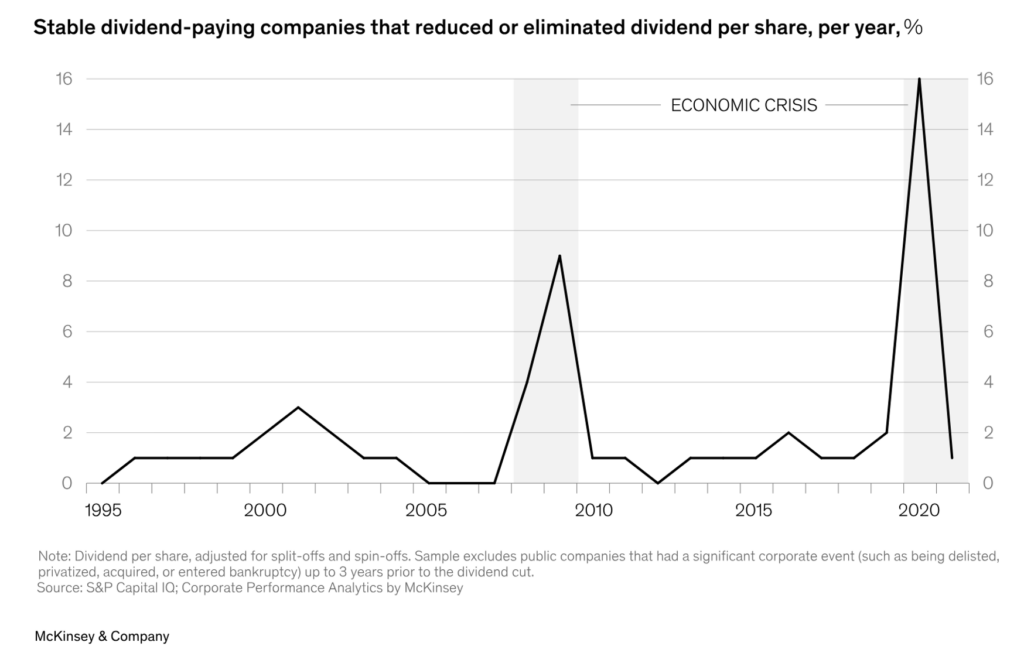

In recessions and other economic downturns, a lot more companies cut dividends. From this McKinsey analysis, more than 8% dividend-paying companies had cut their dividends in 2008-09 crisis. And more than 15% cut dividend during the 2020 shutdown.

One could just focus on companies that historically have been consistent in paying dividends and growing them every year. The downside is that many of them are well recognized by the market and as a result trade at premium.

In the middle of the pandemic recession, I did a blog post in May 2020 on dividend paying companies. I pointed out then that 83 public companies had suspended dividends that year, and another 142 had reduced them. And yet, a vast majority of my own dividend payers had continued to pay unchanged that year.

The key is to find wonderful businesses that are strong enough to withstand economic crises without having to cut their dividends. At the same time, we could also find wonderful businesses in the non-dividend-paying bucket. We don’t get any cash dividends from them, but they also do well in tough times and recover faster.

So perhaps a better strategy is to invest in strong businesses regardless of dividends. And if your portfolio doesn’t produce enough yearly income you require, you can supplement it with some homegrown dividends (Ken Fisher’s term). Both Warren Buffett and Ken Fisher advocate this approach: Liquidate a small fraction of your portfolio to generate income. In May 2018, I wrote this about Warren Buffett’s approach:

His approach is to just sell a certain percentage of shares every year. One can precisely control how much to sell – depending on his income needs. The rest of the money keeps compounding tax free.

This is the approach I follow.

How much is safe to sell from your portfolio? One big concern with selling-some-shares-to-create-dividends approach is what happens when a bear market strikes. When your stocks are down 20 – 50%, is it still OK to sell a fraction quarterly? Yes, but only to a degree.

This is where the 4% rule of thumb comes into play. It is safe to withdraw up to 4% of your principal every year, with the withdrawal amount adjusted upward each year based on current inflation. With the caveat that most of your principal is invested in stocks (not bonds, not cash).

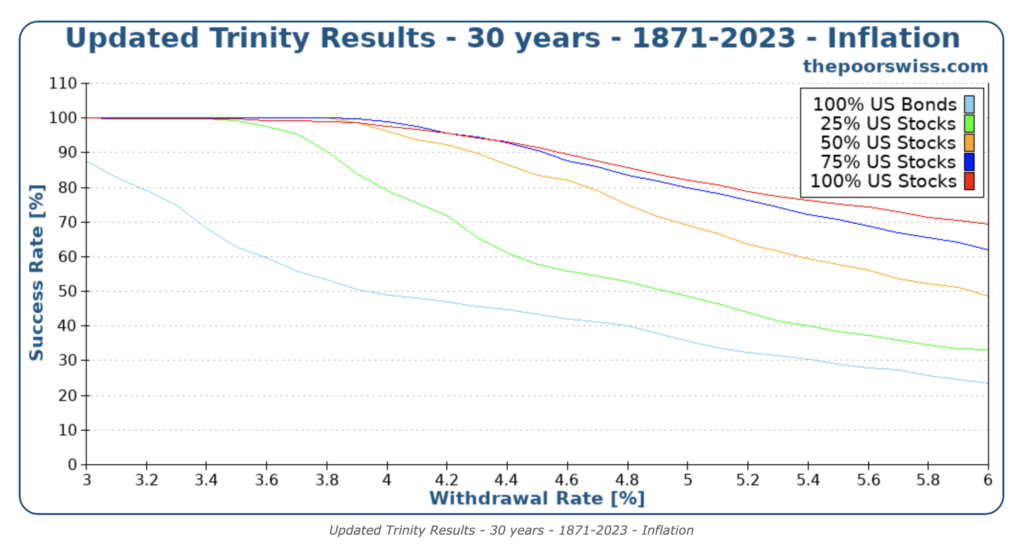

If you want to see more details of how this rule came about, check this excellent Trinity study for more details. The gist of this study is that your capital will last 30 – 40 years if you only withdraw 3.5 – 4% from it every year. Higher stock allocation increases your chance of success.

It is unlikely that you can get 4% or higher dividend yield from your stock portfolio from the get-go. For context, today the top 500 stocks (the S&P 500) have a combined yield of about 1.3%. It is low given stocks’ high valuations today. However, even the 20-year dividend yield has been less than 2% historically. And the S&P 500 consists of some of the best US companies out there. See this chart. The only time in the last 20 years that div yield had gone above 4% was during the 08 – 09 economic crisis.

One could reach for higher yield by concentrating on utilities, REITs, MLPs, etc. but these come with the usual downsides: low growth in dividends and/or share price, higher interest rate sensitivity, and risk of sector/industry concentration. Over the long run, ETFs that yield 4% or higher haven’t kept pace with the overall market performance when we consider total returns (i.e. dividend and share price gains combined).

Perhaps a better approach would be to find growthy businesses that have low yield today but expect to grow dividends rapidly as their businesses grow. These are the kind of dividend-payers that I prefer to own in my portfolio.

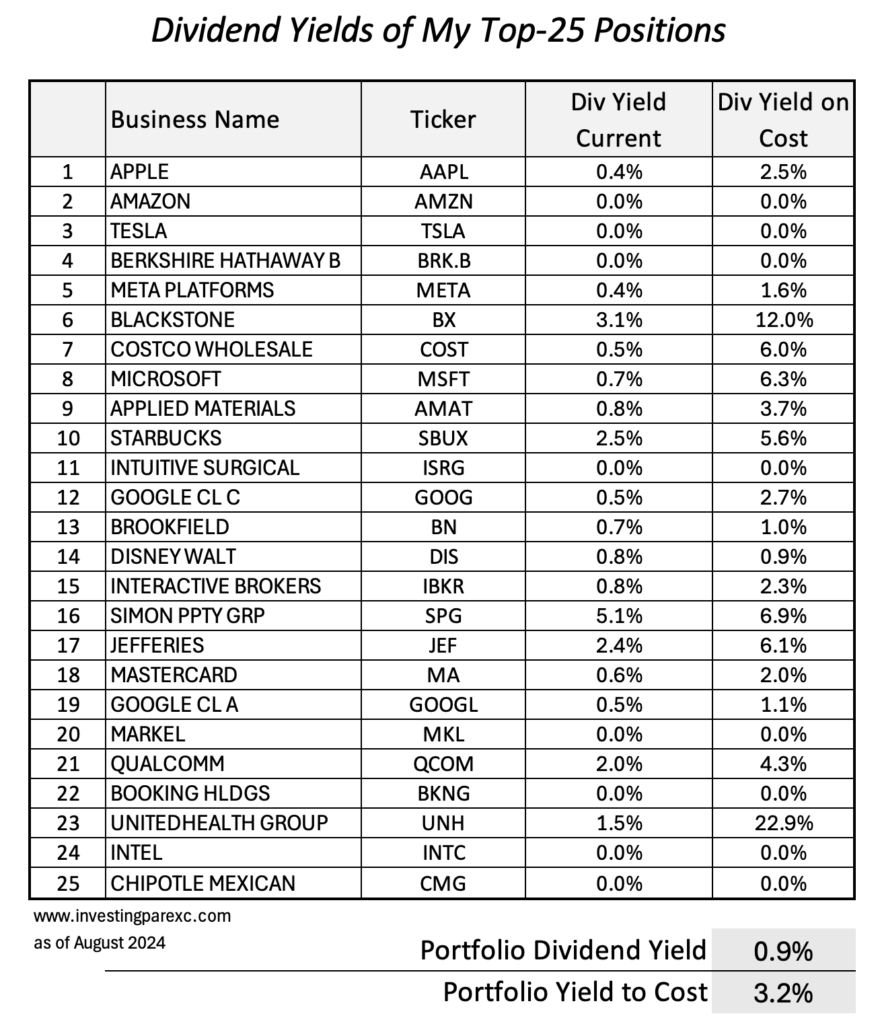

The table below shows my top 25 positions and their individual yields, both current and relative to my cost bases. As I pointed out before, my portfolio has both dividend-payers and those that don’t pay any. Most of my payers are those that started out with low yields but then grew them at a rapid clip over the last 5 – 10 years. This is evident from the differences in their current yields and yields-to-cost. My portfolio’s weighted-average div yield today is only 0.9%, but my yield-on-cost is nearly four times higher at 3.2%. Over the years, some of these businesses have done very well and consequently both their dividends and share prices have risen since.

Some investors also use bonds and annuities to supplement portfolio income. I don’t. I only focus on equities and cash. Today I have about 85% equity and 15% cash.

If you add bonds to your portfolio, be mindful of the effects of long-term inflation. Stocks provide the best long-term protection against inflation even though they are more volatile in the near term. Go back to the graph from Trinity simulations that I showed earlier. You can see that the chances of running out of capital in 30 years increase substantially as less money is invested in stocks.

If you are an investor who is seeking dividend-paying stocks in the hope that they will be less volatile (i.e. safe), think again. As I showed earlier, dividend-paying stocks are not necessarily safer. In economic downturns, they suffer nearly as much. Instead, you should seek out strong businesses, regardless of dividends.

While there is some evidence that high-quality dividend growers (e.g. the S&P 500 Dividend Aristocrats) outperform the overall market during downturns, their long-term performance is about the same. By focusing exclusively on dividend payers, we’d be missing out on other wonderful businesses (60% of the US stocks) who do not pay dividends yet.

If you are an investor who is seeking income from your portfolio because you are either retired or need to supplement other sources of income, follow the 4% withdrawal rule. It won’t matter whether you generate income through dividends or by selling fractional positions (or some combination of the two approaches), your total withdrawal amount during the first year must not exceed 4% of your portfolio. Every subsequent year, you may increase your withdrawal amount by inflation.

To recap, my investing is based on following these principles:

- Buy wonderful businesses and hold them forever (or until they cease to be wonderful)

- Keep generous amount of cash for dry powder investing, rainy day needs, and peace of mind. Amount set aside is based on personal risk tolerance level.

- Stay dividend agnostic – good businesses can be either dividend-payers or not

- If dividends generated by my portfolio do not fully cover my needs, I supplement them by selling fractional positions periodically (within the 4% limit)

If I were an index investor (like I was 15 years ago), my approach would still be similar. I’d invest in low-cost broad market index ETFs (like Vanguard Total Market ETF: VTI) and avoid dividend-only ETFs like the S&P 500 Dividend Aristocrats (NOBL) or Vanguard Dividend Appreciation (VIG)

However, there is no one approach that works for everyone. If you go heavy with dividends, you may lose out on some portfolio growth. But you do have a bit more peace of mind perhaps; those quarterly checks can be reassuring, especially in a down market.

The alternative approach that I follow is to be dividend agnostic and hopefully my stocks will grow earnings and dividends nicely over time. I expect a bit higher volatility in my portfolio but also faster growth.

Leave a Reply