As the market teeters at the edge of another correction (so what else is new!), as always, we stand ready to take advantage of low prices whenever they come. My dry powder coffers are now full. Over the last 12 months, I took all the cash out of my portfolio that I had invested in the 2022 bear market. And some.

I was going through some old notes that I took in early 2020. Back then, I had just met a couple of investors who were keen on buying individual stocks. They said they had cash sitting on sidelines, ready to take advantage of any market pullback. And yet they all failed to pull the trigger in March-April of that year when the COVID struck, and stocks were down as much as 35%.

Why? Because it is not easy to go against the crowd. To do what no one else seems to be doing. When the future appears highly uncertain. And when the media is replete with dire outlooks.

In my investing career, I rarely find people that can go against the grain and have the courage to put their own money in stocks when things look bleak and uncertain. What kind of people are capable of doing that?

- Those who are predisposed to being skeptical of prevalent and conventional wisdom, and

- they study the history of the stock market and believe in the strength of the US economy

It’s true, investors with contrarian streaks tend to do better when investing in an uncertain world. Those who look at conventional wisdom with suspicion. Howard Marks calls it second-level thinking. Here’s an example he shared once:

First-level thinking says, “The outlook calls for low growth and rising inflation. Let’s dump our stocks.” Second-level thinking says, “The outlook stinks, but everyone else is selling in panic. Buy!”

The courage to invest in uncertain times also comes from having studied the markets, recognize patterns in its behavior, and believe in the long-term resilience of the economy.

Here’s a relevant market history lesson, courtesy of Morningstar, What We’ve Learned From 150 Years of Stock Market Crashes

This chart that I have copied from the Morningstar article shows 150 years of US stock market returns, dating back to 1870s. Note all the market corrections and bears that the market had endured since then. And despite it all, stocks exhibited a relentless rise throughout. When we zoom out to this level, all the market dips and dives appear immaterial. As the country’s GDP grew, its businesses and therefore its stock market also grew, albeit with higher volatility.

When we look at the market through this lens, today’s market volatility looks very insignificant. Notice how the COVID bear market of 2020 barely even registers on this chart. To drive this point further, I’ve added a 40-year time-span measure to the chart. 40 years is just about the typical earnings-savings-investing period of an individual investor (a 25-year joins the workforce and earn-save until 65). Slide this element anywhere over the chart, you won’t find a period where the end-of-period market valuation wasn’t higher than the starting price. In other words, no investor lost money in stocks had they stayed the course for 40 years. No matter how many times the market turned lower. If anything, because they were saving and investing throughout their earning career, most individuals would do far better than the chart implies. It’s dollar cost averaging at work.

In a previous blog post, I wrote that since the World War II, the US market only had two rolling 10-year periods with negative returns. But the investors could still have made money in those periods if they were consistently investing. See the data here.

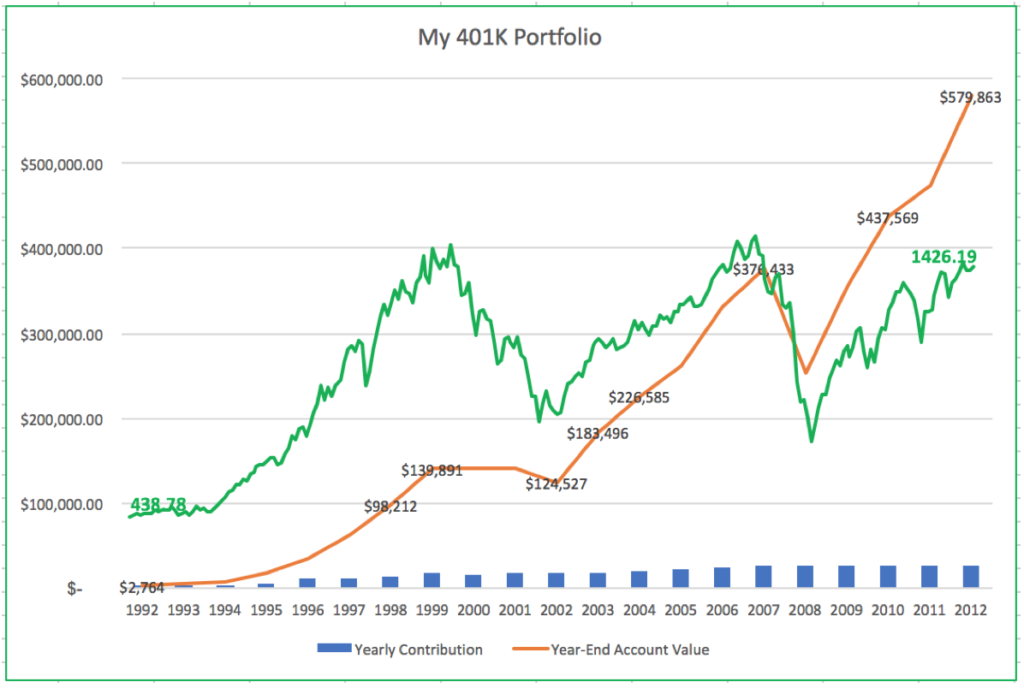

This is not just a hypothetical. I went through a similar earning-investing period where I was dollar-cost averaging into stock mutual funds (in my 401K account) for twenty consecutive years. This period included the so-called lost decade of 2000-10, as labeled on the chart above. But because I was buying stocks as they dropped, my portfolio easily overshot the performance of the nominal stock market of that period. See the chart below.

I was also DCAing into a Schwab index fund from 1996 to 2006 when the market went through the Y2K boom-bust cycle. The market limped to its prior peak in 2006, but my investments had already gone much farther. You can see that chart here.

Today I invest in individual stocks instead of stock funds/ETFs and I use a dry powder strategy to buy during down markets. My investing situation is different now (I’m no longer generating excess savings to invest every month) but the underlying investing principle is the same: Stay invested and take advantage of low prices because the markets eventually will recover.

Returning to the 2020 bear market, it was unknowable at the time how long the pandemic (and the market drawdown) would last. If the history were any guide, it could have easily taken us several years to recover from it.

Knowing that, would you as an investor have dared to put any new cash into stocks at that time? Did you? It is easy to say with the hindsight that we would have. But it’s an entirely different thing to have pulled it off while in the middle of it.

We tend to focus on whether an investment decision turned out to be right or wrong rather than the degree of conviction justified by what was knowable at the time.

- Source: https://www.scuttleblurb.com/

Today, when I meet some fellow investor who claims to be long-term minded, I ask: Did you put any money in stocks in 2022?

It is perhaps also a good time to take stock of experts’ views. How many of those talking heads on CNBC were encouraging investors to buy stocks in ’22? Or were they mostly going with the news flow. In other words, were they all just first-level thinkers?

Hi MC

I agree with all of this

My one concern is the inability of the US to make any serious inroads on the budget deficit and the huge US debt

While the US has a major advantage in being the world’s reserve currency, with no reasonable alternative, are you not concerned that the US deficit and debt will eventually overwhelm the US economy and with it, the public US companies that generate such huge wealth

Countries which have failed to maintain control over inflation or budget deficits have eventually collapsed with disastrous consequences; but none as large and wealthy as the US

Of course if this did happen to the US, the consequences for the rest of the Western world would be severe, although China and Russia would no doubt be delighted

What are your views on this – and whether it affects your investment strategy

Hi, thanks for commenting. I mostly ignore macro concerns in my investing but with one general exception: I believe that US will continue to remain a great place to invest for the future, even with many fiscal or monetary issues that prevail today.

Mr. Buffett said it well in his recent (2024) shareholder letter:

“Paper money can see its value evaporate if fiscal folly prevails. In some countries, this reckless practice has become habitual, and, in our country’s short history, the U.S. has come close to the edge… Businesses, as well as individuals with desired talents, however, will usually find a way to cope with monetary instability as long as their goods or services are desired by the country’s citizenry… Berkshire shareholders can rest assured that we will forever deploy a substantial majority of their money in equities – mostly American equities although many of these will have international operations of significance.”

I’m in Mr. Buffett’s camp. The whole section “Where Your Money Is” from his letter is an excellent read: https://www.berkshirehathaway.com/letters/2024ltr.pdf

Good Day EMCEE,

Thank you for your post. I am a long time follower of Investing Par Excellence and wanted to ask if you’ve explained in the past, how you go about selecting individual stocks.

I did buy in at the depth of the COVID recession and just went with my “gut” as to what companies were promising investments. I have NOT regretted that decision and in fact, bought more individual companies a few years later, once I saw the results versus my SP500 fund.

If I’m honest, being a low cost indexer is comforting due to the diversity factor, but when I research the SP500 on any given day, it’s quite common to see that 1/3 or more of those listed are returning negative YTD (my source is Slick Charts) – especially at this time.

Still, picking winners can ultimately be difficult if not impossible in the short term. So this brings me back to my initial request. Can you give a nail-biting indexer some how to steps as to picking stocks for the long term.

Thank you for sharing your thoughts. I always look forward to your posts.

Be well.