I do some tax planning every year – usually in December. It is a yearly ritual that I am accustomed to. Fortunately, my taxes have not been very complicated since, most of my working years, I didn’t have any business income. So, no large business expense deductions, asset depreciations, or pass-through income to deal with. My year-end tax planning revolves around tallying employment income, maximizing deductions, and timing capital gains/losses. Things that are mostly done on Forms 1040 and Schedules A, B, and D.

I do some tax planning every year – usually in December. It is a yearly ritual that I am accustomed to. Fortunately, my taxes have not been very complicated since, most of my working years, I didn’t have any business income. So, no large business expense deductions, asset depreciations, or pass-through income to deal with. My year-end tax planning revolves around tallying employment income, maximizing deductions, and timing capital gains/losses. Things that are mostly done on Forms 1040 and Schedules A, B, and D.

This year is turning out to be a bit different though. The upcoming tax changes could potentially take effect as early as next year. Regardless of how you feel about the tax proposal itself, its inevitability appears to be in little doubt – given that both chambers of the Congress have passed their own version already. And the two bills are very similar.

So this year I am going with the assumption that the proposed tax changes will be signed into law for the tax year 2018. From what I have seen so far, there are some key changes that will affect investors like me. But before we dive into the proposed tax law impact, here are three end-of-year steps I take this time every year:

- Maximizing retirement account contributions: Most years I am not qualified for either Roth IRA or Traditional IRA contribution (income too high). Nevertheless, I run a quick check in December to see if I am allowed to contribute to them. Whenever I am eligible to contribute to a 401(K), I make sure I max out there too. The real deadline for IRA contribution is the tax day the following year (April 17 in 2018). But for most 401(K) plans, December is the last month where you can make a contribution. Turns out that this year, as expected, I can’t make either IRA or Roth IRA contributions.

- Harvesting tax losses: December is also good time to take stock of any capital gains and losses in the year. Of course, this only makes sense for taxable brokerage accounts – and not the tax deferred accounts. In my taxable accounts, I mostly have individual securities. My mutual fund investments are in retirement accounts. This year I have realized some capital gains but I don’t have many candidates for harvesting losses. I do have some losses in oil & gas stocks but their cost bases today are low. I had realized losses in them last year and then bought them back after 30 days to avoid the wash-sale rule. Chipotle Mexican (CMG) is the only stock that I am considering selling this month to harvest losses. I am down about 30% from my cost basis.

- Tallying up itemized deductions. I usually end up itemizing my deductions. Between property tax, sales tax (since Texas does not have income tax), and charitable contributions, I have enough deductions that easily exceed $12,700 standard deduction (for married couples). I also have some mortgage interest to deduct but it’s not as big as my property tax bill. I do a quick check via TurboTax to make sure that my itemized deductions are high enough to justify itemizing them.

Learn to do taxes!

Investing is more than just picking stocks and bonds. Good investors aren’t concerned about maximizing their portfolio’s nominal returns – they are focused on after-tax returns. If you are a self-directed investor (or aspiring to be one), it helps if you understand how your income and capital gains are taxed. You’d be able to make better decisions for your investment portfolio. I have been doing my own taxes for years. I use Intuit’s Turbo Tax software. If your income is mostly from employment then taxes are really not that complicated to figure out. Even for more complex scenarios, Turbo Tax makes them easier.

I also use prior year’s Turbo Tax to do what-if analyses. It’s so much easier and faster than doing it manually or via a spreadsheet. It is also more cost effective than hiring a Tax CPA to do it for you.

Since I do my own taxes every year – I always have prior year’s Turbo Tax handy to use. I am also knowledgeable enough about taxes to know what data to enter. Using last year’s Turbo Tax is quick and easy method to do what-if analysis – albeit not 100% accurate.

Those were my standard year-end rituals. Now let’s look at what 2018 might bring. There are a few items that I know could affect my taxes next year:

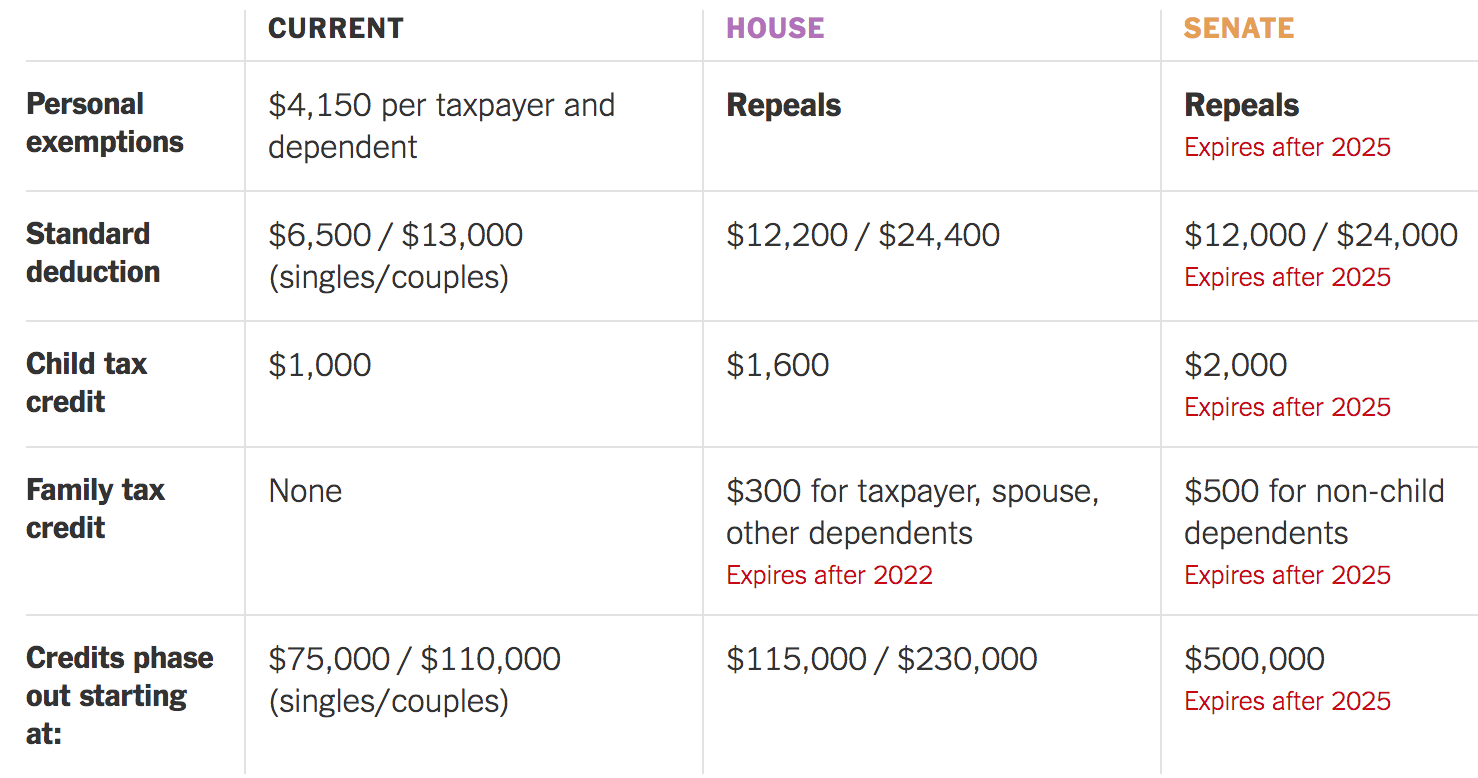

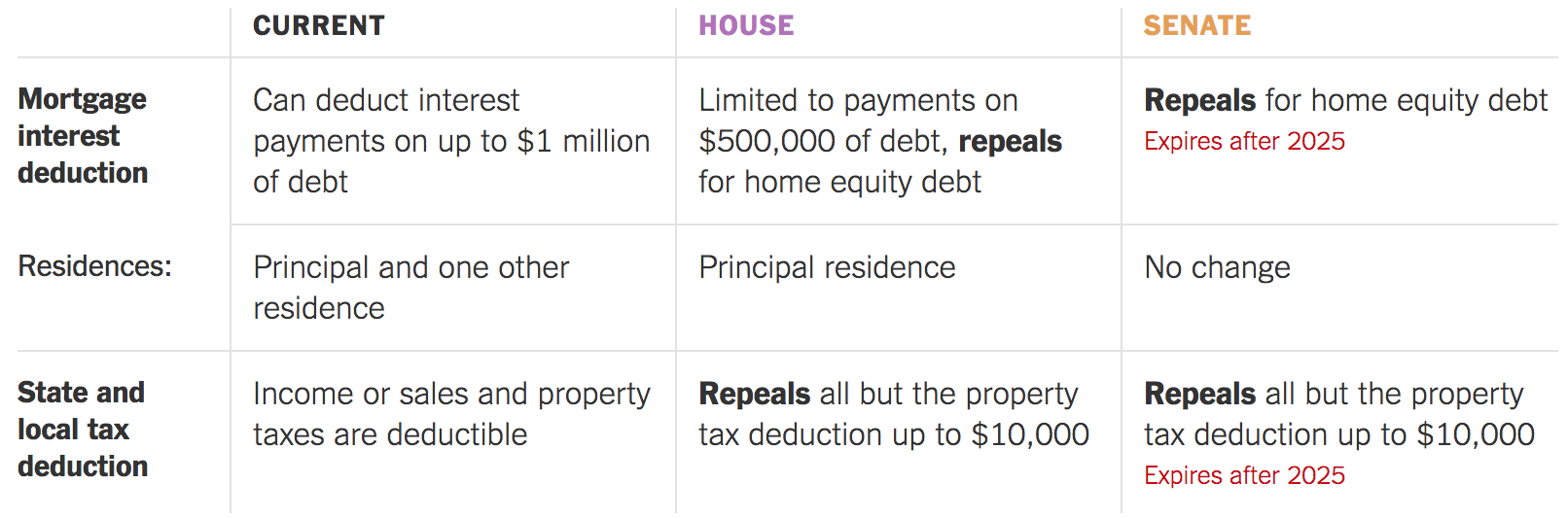

- Standard deduction could be doubled to $24,000

- Property Taxes deduction could be limited to $10,000

- State & local tax deduction could be eliminated

- Mortgage interest deduction might be limited to $500,000 of debt. Only principal residence.

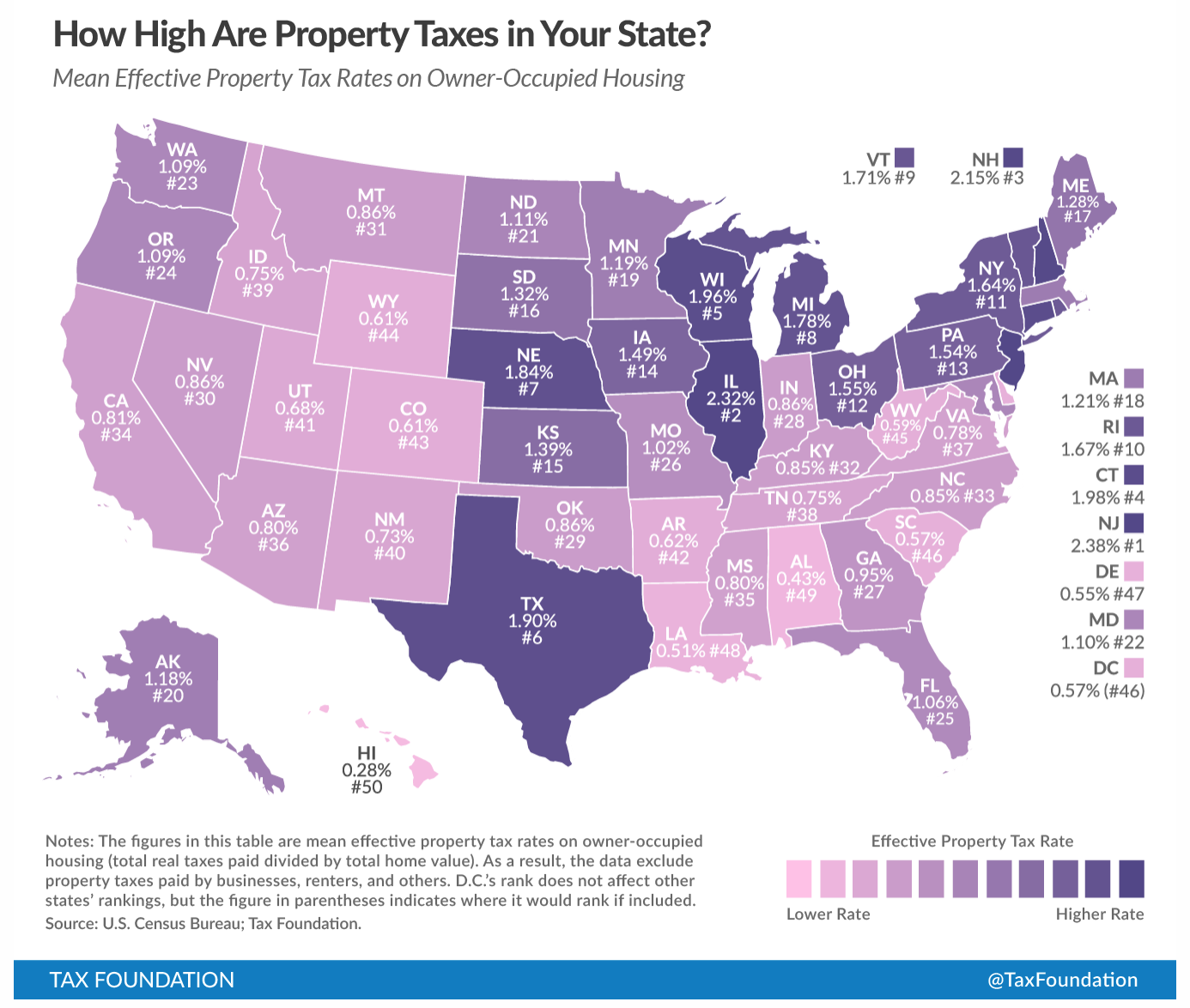

I have less than $80,000 of mortgage left on my house. Mortgage interest is not a big expense for me. Also, Texas does not have any state income tax so no deduction for me there. However, Texas has among the highest property tax rates in the country.

My property tax bill this year is about $12,000. Factoring in charitable contributions and other miscellaneous items, I estimate that my total itemized deductions in 2018 could be around $25,000. If standard deduction were to double next year and with property tax being capped at $10K, chances are I won’t get a big benefit if I itemize next year. In my case, it’d be better if I could pull in those 2018 deductions into 2017 where I know I can itemize. And then just take standard deduction next year – hopefully it would be double the amount it is this year.

So that’s what I plan to do this year. I will be paying up my 2017 property tax bill this month (December) even though it is not due until January. I paid 2016 prop tax in January this year – so I can claim deduction for both tax bills in my 2017 returns.

I will also be pulling in my 2018 charitable contributions to this month. For some years now, I had stopped writing personal checks to charities. Instead, I have a Donor Advised Charity Fund with Schwab Charitable.

Why Use a Donor-Advised Fund for Charitable Giving?

From an investor’s perspective, there are two major advantages in opening a Donor-Advised Fund (DAF).

Avoid capital gain tax. If you have appreciated investments (securities, real-estate, etc.), why sell them, pay capital gains tax, and then donate remaining cash to charity. Rather, you can donate your investment directly to your DAF and then have the DAF write a check to your favorite charity. This way, you will avoid paying any capital gains tax. The fair market value of your assets will be fully tax deductible if you itemize.

You could do the same thing if the charity is capable of processing in-kind donations like stocks. I’ve found, though, that many smaller charities that I regularly donate to aren’t set up to accept in-kind gifts. They will happily take a check from my DAF instead.

Having a DAF especially comes handy in times like these. We have had a bull market for several years. Long-term investors like me have appreciated assets in our brokerage accounts. See my portfolio here. I know I will be making donations to charities every year. Why not take advantage of today’s market and donate some highly appreciated investments to a DAF, take tax deduction on the entire amount today, and then donate over the next two years?

I will be doing that this month. I have already made 2017 donations to my DAF. In light of expected 2018 tax changes, I will also donate 2018’s amount this month since I will be itemizing deductions this year. Next year, I won’t have any tax write-off for charitable donations but that’s OK – I plan to take standard deduction in 2018.

One final note: it’s still possible that the proposed tax changes would not go through after all. Or the final bill might look significantly different than today’s. Or the tax changes wouldn’t take effect in 2018. However, the steps I am taking this month to accelerate deductions into 2017 should still work OK. They might not amount to much tax savings if larger standard deduction or capping property tax deduction do not make into the final bill. My 2018 tax bill might end up a bit higher than I expect today. On the other hand, I know for sure what my 2017 tax will amount to. It will get the benefit of additional property tax payment and charitable contributions. Worst case, the expected savings in my 2017 tax bill will be entirely offset by a proportional increase in my 2018 taxes. I can live with that.

[…] 2017 12 11 my year end tax moves […]