About a year ago, I had opened a hedged Apple (AAPL) position. The goal was to invest cash in an asset where I could benefit from the upside but also limit my downside risk. The cash I had invested was my dry powder cash—the kind of cash that I would need some day to buy stocks with. I first wrote about this hedged bet in March last year. Seven months later, I wrote again about it and pointed out that the Apple stock had already well exceeded my upside limit. As I wrote then, I chose not to close the position at the time. I had wanted to let the time-value of my position decay further so it would be more profitable to close.

Well, I finally closed this position last month (on March 12th). It was a 27-month long position that I ended up closing in twelve months. What forced my hand? This coronavirus induced market crash. No regrets though. As I wrote in that first blog post, this hedge replaced a bond position in my portfolio that had returned a meager 2.5% (annualized) in five years. So, last month when I closed this Apple hedge, my return amounted to about 13% annualized and pre-tax. Not bad for a year-long position with little downside risk.

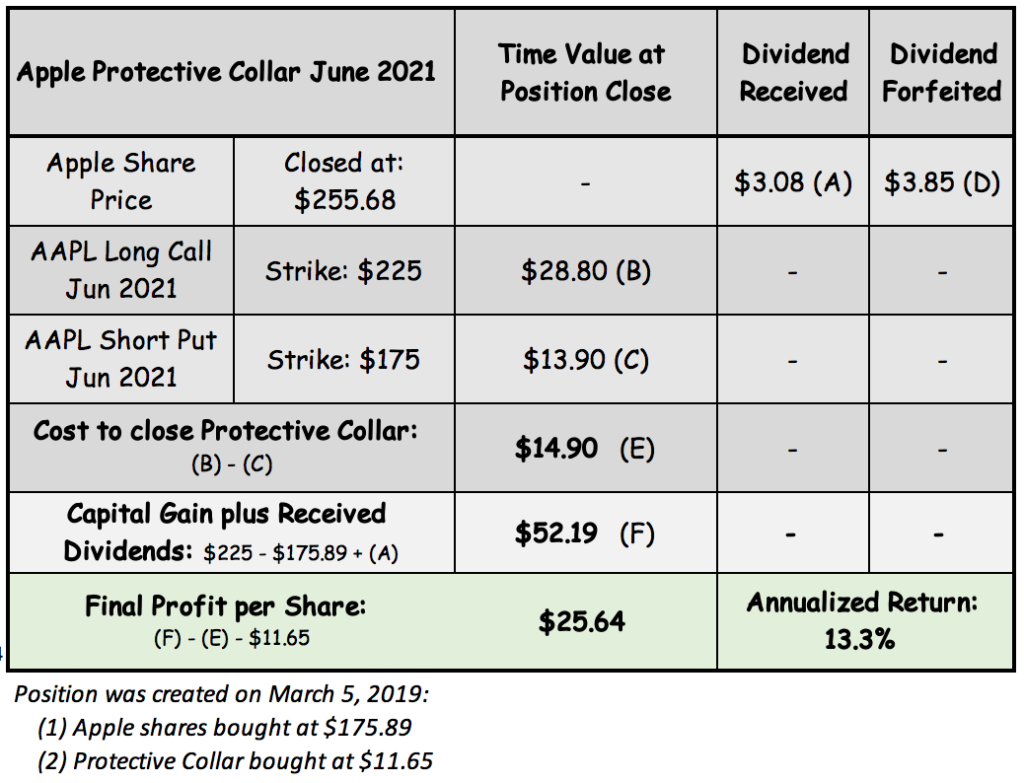

Had I kept the position until its final maturity in June 2021, I would have gotten maximum 9.8% annual return. Lower return than what I made, but it would have been higher in terms of total dollar amount.

I closed the position because I needed the cash. The market was in the midst of a severe decline and I was ready to deploy cash to scoop up some bargains. This hedged position was one of several that I closed last month to generate dry powder cash to invest. See my post from March 17th for what I bought with the cash.

I feel good about what I bought last month. Those are all durable profitable businesses run by strong managements. I think I got them at good prices too. While I could have earned more had I kept this Apple hedge around for another year, this tradeoff was a no-brainer.

The Numbers: I closed the position when Apple shares were trading at $255.68. Since my upside was capped at $225, I received $49.11 per share capital gain. I also collected $3.08 in four dividend payments. The cost to buy out the hedge prematurely was $14.90. My overall profit was $25.64 per share. I had bought 500 shares, so my total dollar profit was $12,820. See the detailed breakdown in the table below. Also refer to my first blog post for initial cost breakdown.

When I wrote the last post on this in October, I had estimated that I could earn around 13% return if I close the position in six months. It turned out that I ended up closing the position in five months but with just about the same overall profit.

Back then I could not have envisioned this sudden and massive market meltdown. No one could have. In January this year, I wrote about Barron’s annual January gathering of market pundits, called the ‘annual roundtable’. I called the event somewhat disparagingly ‘another weekend of worry’. The market gurus waxed eloquently about how the market would behave this year. The general mood of the panelists was cautious but upbeat. One panelist had even forecasted how stocks would move in the first half of the year and then change direction in the second half.

With the hindsight, how good were those predictions? They were probably not even worth the ink they were written with. And therein lies a lesson for all of us long-term investors. We must not pay heed to market (or economic) predictions. The future is unknowable. Two things that we do have control over though: One, belief in the long-term prospects of the economy. As Peter Lynch aptly pointed out in a Barron’s interview in December:

The thesis underlying everything, whether you’re an actively managed fund or a passive fund, is that the U.S. will be OK. If you don’t believe that, you shouldn’t be in the stock market.

Secondly, we must always plan ahead for market turbulence. It’s a regular occurrence. We just won’t know when it might happen. For this, I keep dry powder cash in my portfolio. If and when the stock market goes into a panic, I will be ready. Well, it turned out I was indeed ready last month.

Hi MC

These last few weeks have been a classic case of the wisdom of the mechanical dry powder strategy

Prices and indices have moved fast and that tends to make decision making more difficult, as there is always a temptation to “wait and see”

It is hard to understand how the market can respond so positively when earnings for Q1 for many companies are likely to be poor and Q2 abysmal – there seems to be a disconnect between earnings and valuation.

The fed can provide liquidity and back stop credit, but it cannot generate demand

Personally I think there will be another test of the lows recorded in March sometime during the summer when earnings are released, but that does not seem as likely as as a week ago

we shall see

Nicholas

Hi Nicholas:

Indeed the market could see another low down the road before recovering. Howard Marks of Oaktree fame wrote this in his latest memo: “After the optimistic buyers of the initial dips have responded to the low prices and bought, the pessimists find the new, higher prices unsustainable and engage in another round of selling. And so it goes for a while. ”

As for me, if the market drops below 35% mark, I will be ready to deploy more cash. I have 30% dry powder left. Let’s see how it goes.

https://www.oaktreecapital.com/insights/howard-marks-memos

Thanks MC

yes some good material in Howard Mark’s memos – thanks for the link

Hi,

Not everyone has the means to keep significant cash on the sidelines for this. I just started investing but mostly just via my 401K paycheck deductions.

Hi Jeff: Good point! I used to be the same when I was younger. I wrote about it in another post how I dollar-cost averaged into a 401(K) for 20 years. It is another great way to invest. Any market dips, and your new dollars will buy you more shares. Going through a bear market while keeping faith in the long-term compounding of stocks can be difficult—but it can also be very rewarding. I wrote about it here: https://www.investingparexc.com/2019/10/01/bear-market-curse-or-blessing/

Also see this: http://www.investingparexc.com/2017/11/02/my-401k-story-from-1992-to-2012/