Two years ago, I did a blog post on Blackstone’s real estate investment trust called BREIT. It had just opened its doors to retail individual investors like me. At the time, I was looking to increase my investments in commercial real estate (CRE) assets and thought that it was a promising opportunity to dig into. Here’s that post from April 2018.

I spent a couple of weeks investigating BREIT. I went through the prospectus, its fees structure, and the investing approach. I even talked to my brokers at Fidelity and Schwab about placing a trade.

But in the end, as I explained in that post, I decided against investing in it. My decision had nothing to do with the quality of the offering or the reputation of its manager. In fact, I had high regards for Blackstone (BX), its fund manager, then, and I still do. My main issue was the level of fees (upfront sales load and wrap-fee service charges) I had to pay to invest in the fund. I considered it too high and thought I’d be better off investing my capital in other real-estate alternatives (such as publicly traded REITs). Read that April 2018 post for details on BREIT fee structure.

In this post I will be reviewing BREIT’s performance. Three and a half years have passed since BREIT was founded by Blackstone. It started gathering funds in January 2017 but did not start paying monthly distributions (aka dividends) until three months later.

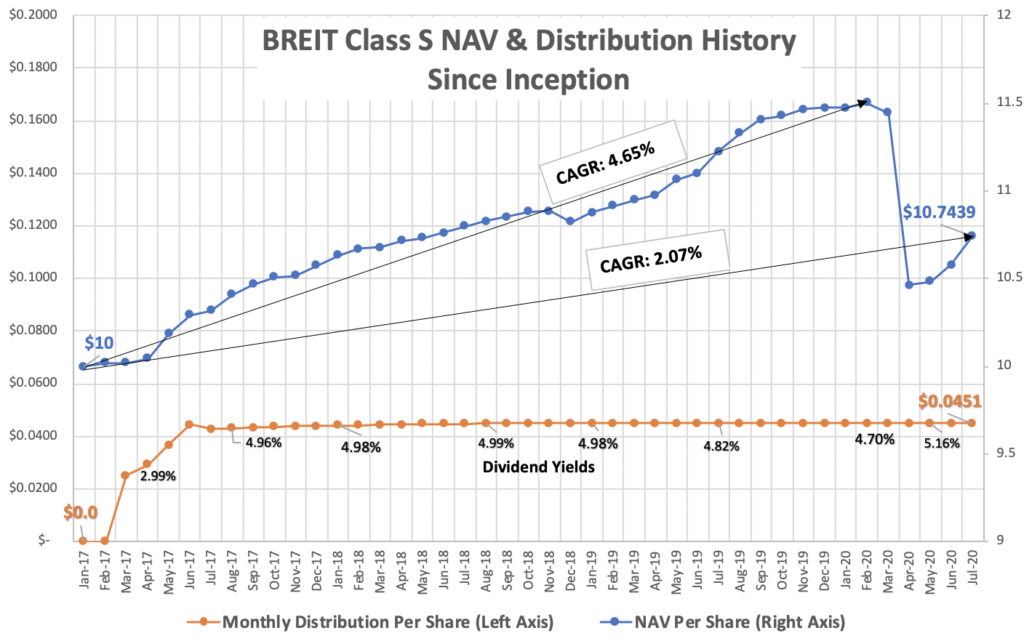

This graph shows BREIT monthly cash distributions and NAV (net asset value) estimates since inception.

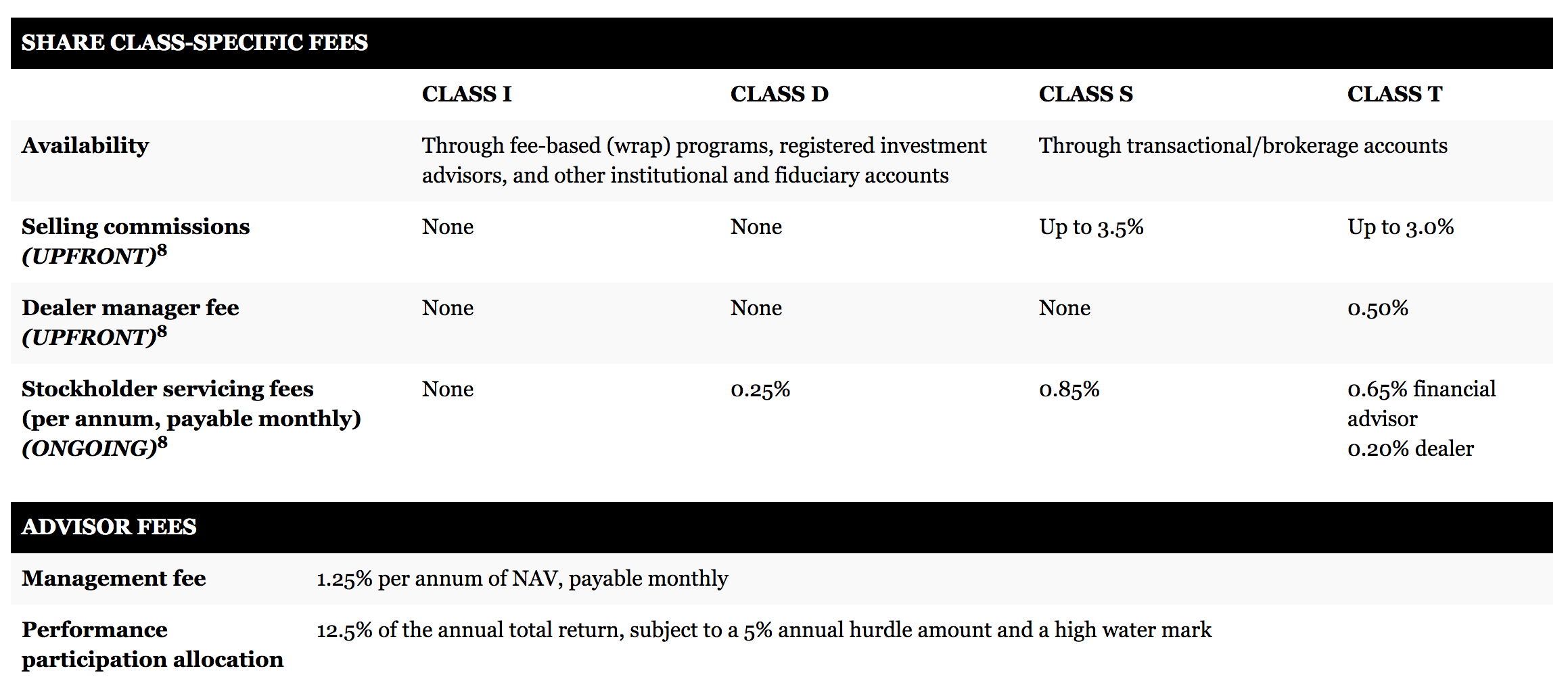

I picked Class S shares to compute BREIT performance since it is one of the two share classes [the other is Class T] readily available to brokerage accounts. Class S has a one-time sales commission of 3.5% plus on-going 0.85% annual service charge. [See this chart from the 2018 blog post on four BREIT share classes.] If an investor has his money managed through an advisor, he could possibly buy one of the other two share classes that have no upfront sales load. But it will amount to roughly the same thing since he’d be paying advisor fees instead. If I were to invest in BREIT, I will need to go with Class S shares since I manage my own money and don’t pay for a full-service brokerage account.

{kind=link}

As expected for a Core-Plus type REIT, BREIT had steadily grown its NAV since the inception—until the pandemic crisis hit. I estimate Class S NAV growth (through February this year) to be about 4.65% CAGR. In the following two months though, its NAV dropped quickly as future growth in rental income is expected to slow down considerably. Taking this NAV drop into account (and partial recovery since then), its NAV growth to date drops to about 2% CAGR.

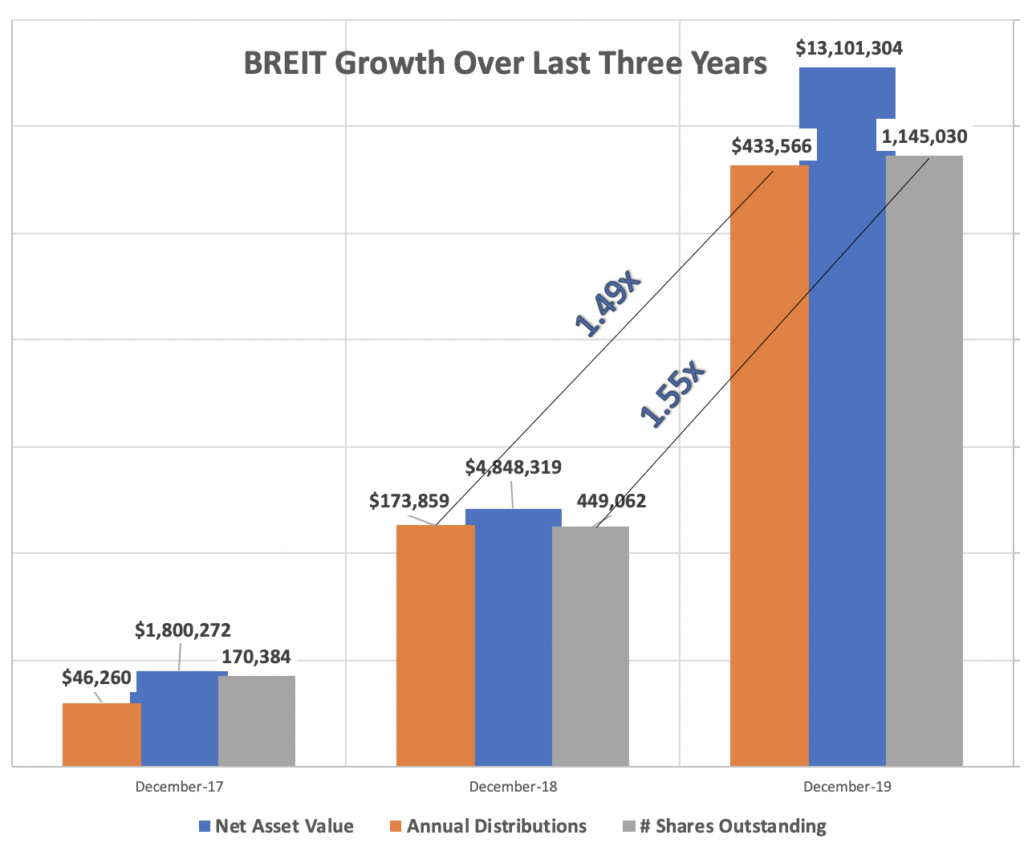

Monthly distribution per share also grew quickly in 2017 but since then it has plateaued. I expect BREIT to keep getting gobs of new investor capital every year and expand its portfolio of properties accordingly. This implies lots of new share issuances though. Take a look at 2018 to 2019 growth in the chart below. Shares outstanding grew by 1.55x while the total distributions increased by only 1.49x. I expect this trend to continue i.e. new share issuances to keep pace with total distributions, resulting in flat distribution on per share basis.

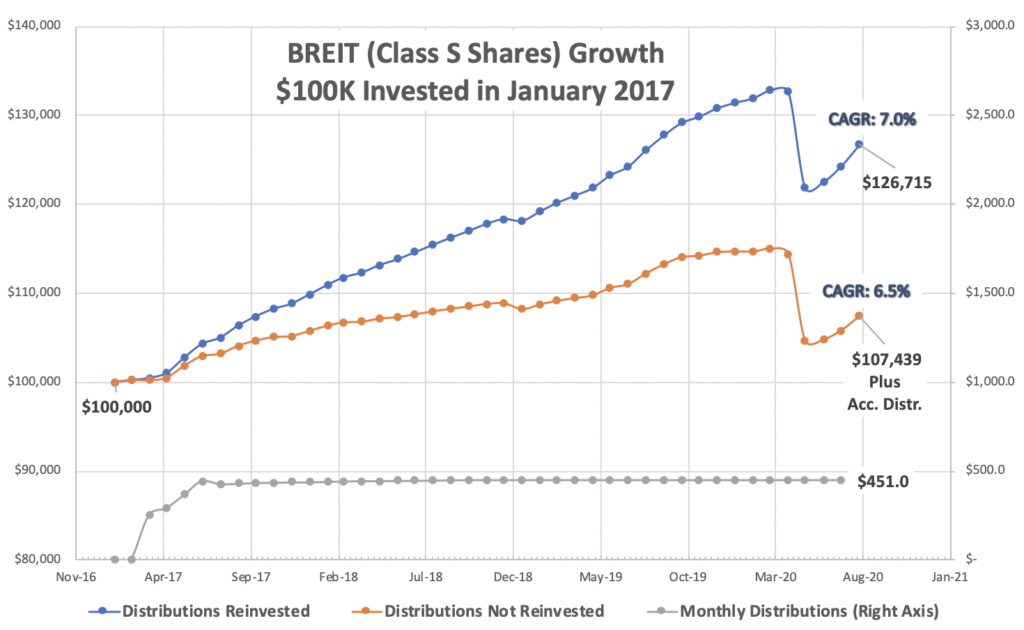

Blackstone’s 2Q2020 earnings report shows that BREIT inception-to-date IRR (internal rate of return) is 7% (Jan 2017 to June 2020) if all distributions are reinvested. I ran my own numbers as shown in the graph below. If I had invested $100K at inception (Jan 2017) and reinvested all monthly distributions, my position today would be worth $126,715 today (July 31st). This indeed amounts to 7% CAGR. But I realize that some BREIT investors would consider monthly distributions as income (to consume, not reinvest). In that case their effective return drops down to 6.5% CAGR.

Why is it called Core Plus? Real estate investments are traditionally put in one of four buckets with respect to their risk-reward tradeoffs. Those four buckets, in order of increasing risk (and potentially higher returns) are Core, Core Plus, Value Add, and Opportunistic.

Core: These are conservative low-risk investments with stable rents and not much growth. People invest them for steady income, not so much for growth. One can consider them bond alternatives. Expected annual return ranges from 6% to 11%.

Core Plus: Still the same kind of high-quality real estate like Core, but with the ability to increase cash flow with some property improvements, re-leasing, etc. Cash flow risk tends to be somewhat higher than Core. So are the possible returns: 8% to 12%.

Value Add: These are moderately high-risk investments where significant cash flow increase is possible with upfront value-add improvements. These properties are often distressed with some existing cash flow. Significantly more risk than Core Plus with potential returns in 11% to 15%.

Opportunistic: This is the highest risk category. These are usually investments in severely distressed properties where there might not be any existing cash flow. Or a property to be constructed or restructured anew. Either way, these investments usually do not generate any income until a turn-around is accomplished. If successful, returns can be very high: often 15% and up.

Returns as of today are somewhat below par (only 7% while I expect a Core Plus fund to generate 8-12%) but COVID-19 disruption is a big factor. If we consider the pre-pandemic period: from inception to February 2020, the BREIT has returned 9.6% with distributions reinvested. 10% annual return is reasonable from a core-plus type fund.

I expect BREIT NAV to recover as the economy moves past the pandemic over the next couple of years. I also expect its returns to revert back to the mean—somewhere around 10%.

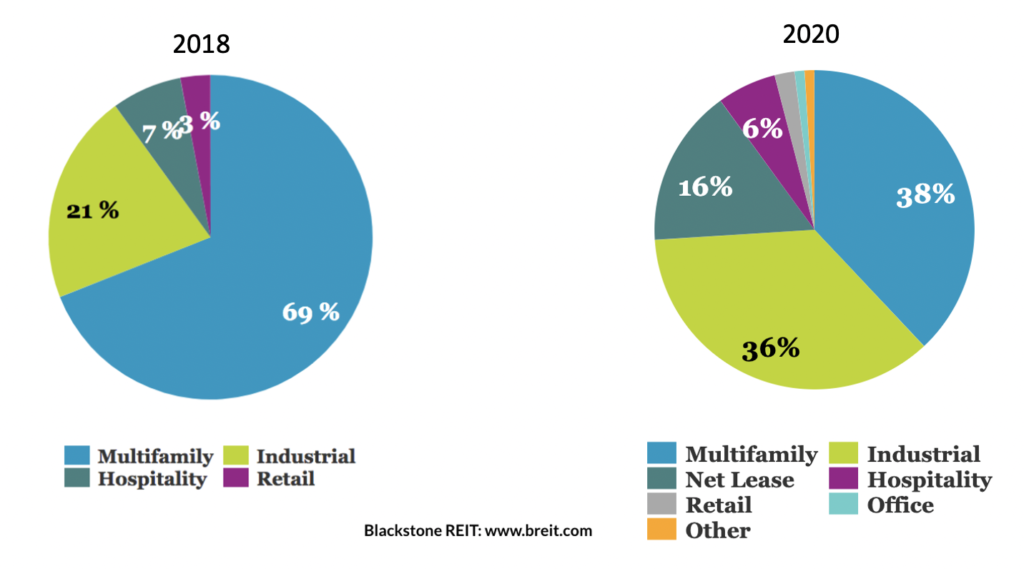

BREIT is a fine investment for people looking to park their cash in a low-risk steady-income fund. It has certainly proven itself over the last three years. It has consistently received new funds from investors every quarter, growing to a near $18 billion asset-under-management today. WSJ reported recently that in 2019 BREIT attracted 73% of all net inflows that went into public non-traded REITs. The fund even reported net new fund inflows in this past quarter when investors were mostly pulling money out of REITs. The fund had started out focusing mostly on multi-family and industrial real estate—both of which turned out to be relatively immune to the pandemic disruption. More recently, it has also branched out into certain iconic net-lease properties in the Las Vegas Strip with very long-term leases and high credit-worthy tenants (Bellagio, MGM Grand, Mandalay Bay).

This chart shows how property allocation has changed in the last two years. Since it hasn’t disposed off many properties in the time period (remember, it is a core plus REIT) the change reflects what it has done with new capital.

I don’t have any doubts that BREIT will come out of the present recession unscathed and do well for the investors. I’d expect nothing less from it given its management is from Blackstone, the veritable top-notch asset manager. See my profile on Blackstone here.

If you are an investor in BREIT, I’d say stay with it. It will provide steady and stable monthly income for you, along with some capital appreciation. I also hope you understood getting into it that it is a low-risk low-growth type safe investment. Granted the recent drop in NAV was a bit unexpected for most investors, but these are unusual times. If anything, today is a good time to put more of your money into it. BREIT properties are valued lower today than earlier this year, and this is an opportunity for savvy patient investors.

I’d also suggest that investors reinvest monthly distributions into BREIT shares, if they can afford to. BREIT provides for a no-cost automated way of doing it. You won’t have to pay any sales commissions. Already, more than 60% of the distributions are being reinvested by the current investors (per 2019 annual report). Over time, I expect BREIT yield will hover around 5% (as it has been since early days) but its NAV per share will grow steadily. We can get greater benefit from this NAV growth if we reinvest in our shares.

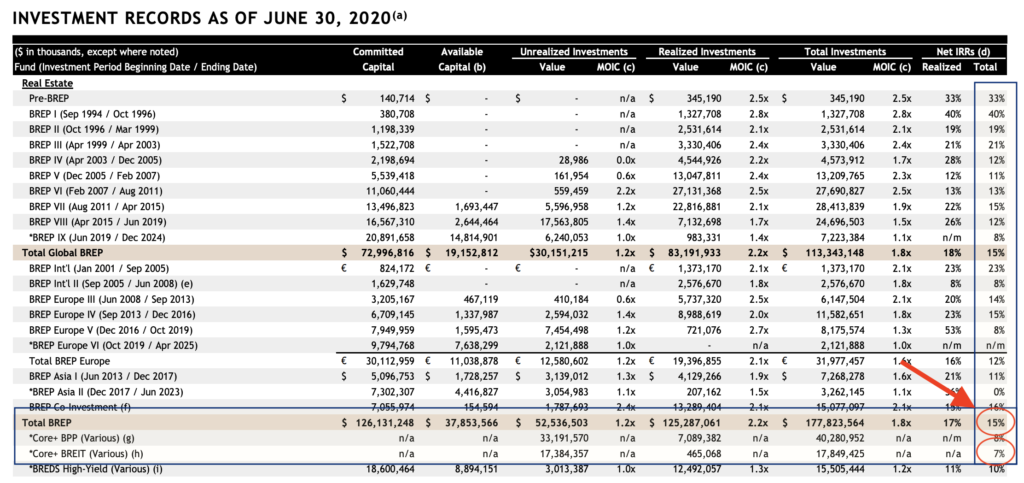

Blackstone: As I had mentioned in my post from two years ago, I chose not to invest in BREIT at the time. Instead, I invested in Blackstone, its fund manager. Blackstone generates more than half of its profits from managing real-estate investments. BREIT is one small part of it. It also has much larger institutional RE funds that invest in Value Add and Opportunistic classes of properties. From the table below, historic rate of return (IRR, net of fees) of Blackstone’s Real Estate Partners funds (BREPs invest in opportunistic real estate) is 15% versus only 7% to date for BREIT fund.

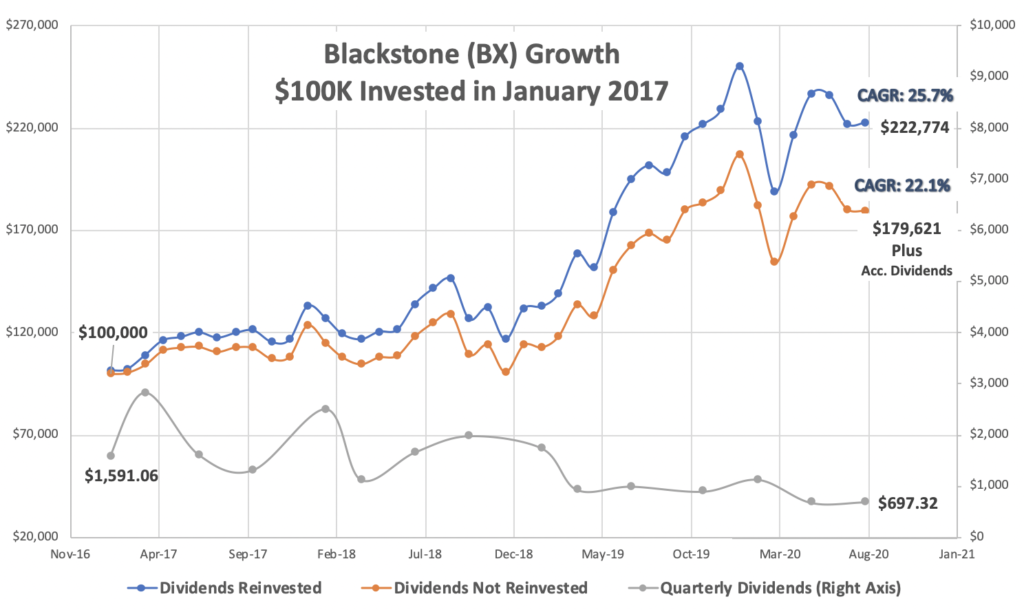

I expect Blackstone to continue growing much faster than BREIT, albeit with greater volatility. Blackstone is a publicly traded security so its share price will always be affected by the stock market fluctuation, as evidenced from the past three months. Even its quarterly dividend amount fluctuates with changing market conditions. As expected with this price volatility, its historic returns are also higher. $100K invested at the start of 2017 would have grown to over $222K today (with dividends reinvested) or $200K (gain plus cash dividends). This is annual growth rate of 25.7% and 22.1% respectively.

I am a patient long-term investor who’s willing to hold on through the ups and downs of the stock market. I consider my Blackstone holding as an investment in commercial real estate since that’s where it gets more than half of its income. So far, investing in Blackstone, the asset manager, has been more profitable for me than an investment in its BREIT fund.

Very well written and researched blog. Thanks. One question, have you done any analysis with personal tax taken into account? Most of the distribution from BREIT would be considered “return of capital” and therefore be sheltered from any income tax, while dividends from public REIT and capital gain from owning stocks are subject to income tax. Do you think it’d put BREIT at an advantage if we measure returns net of income tax?

Thanks for the compliment!

It is true that today majority of BREIT distributions are in the form of return of capital, and thus non-taxable. I believe it’s because BREIT is investing new capital rapidly and depreciation is high from newly acquired properties. How long it would last, I am not sure. I suspect it will be like this for a while.

Two things to keep in mind here: (1) All REITs (public or private) has this “return of capital” feature, so this is not something unique to private REITs only. (2) This return-of-capital distribution decreases our cost basis dollar to dollar. So if/when I sell BREIT shares, I would pay ‘higher’ capital gains tax because my cost basis has gone down.

So, no difference in theory between public or private REITs here. Though, I haven’t done any research on how many public REITs distributions are return-of-capital type. Also the effect is a trade off between paying income tax today versus cap gains tax tomorrow.

Public stocks do not have this provision, true. Public partnerships do. Stocks don’t distribute all their profits any ways – they are allowed to reinvest.

I haven’t considered tax implications for my BREIT analysis. It’s too difficult to consider all possible scenarios. Different tax rates for different income levels, future tax rates versus today’s, retirement account investments versus taxable accounts, etc. If I invest in a REIT in my Roth IRA, all my distributions are tax free.

I am invested in BREIT for about two years and generally OK with it. However, it’s not really a “low-risk” investment as you called it. See the drop this year. Its share price tumbled since March and haven’t recovered yet.

Well, it did drop big time in this Covid scare, no question! I call it low risk because I don’t see its distributions getting affected, even in these times. I expect BREIT to continue to pay quarterly dividend at the same rate for foreseeable future.

With its NAV/share dropping like it did, it’s a concern for those who may be considering bailing out of it in near future. I hope you are not? These non-traded REITs are not really meant for getting in and out frequently. My advice would be to have faith in its long term durability and ride out today’s highly unusual circumstances. Its property values will recover as things normalize.