I found this book at a Costco book stand. I am not a Tony Robbins follower but a quick scan of it made me curious. So I borrowed a copy from my local library.

This is not meant to be a book review though. For some good online reviews of the book, check these two links: here and here. In this post I’ll review some key elements of the book’s investment thesis and also suggest a simpler alternative for potential investors to consider.

Let’s make one thing clear at the outset: I tend to agree with many other online reviewers who found the book more or less a sales job for one specific RIA (Registered Investment Advisor) in which Tony Robbins has financial interest.

But at the same time, I don’t dismiss the book entirely because it provides good intros to various alternative investments that individual investors may not be aware of. It also helps that the two co-authors have dedicated all proceeds from this book to a NY non-profit.

This book is about alternative investments and how investing in them could be beneficial for investors. Alternative investments (or alts) are asset classes that are not considered traditional (not stocks, bonds, or cash): Real estate, private equity, hedge funds, commodities like gold, silver etc. Many of these asset types are generally out of reach for non-institutional investors.

The first half of the book is intros to various alt investments. The second half is interviews with successful investors in each of the alt areas. The authors called them titans of the industry.

The book dedicates one chapter on each of the alt investment type it recommends:

- GP Stakes

- This is what intrigued me at first since I didn’t realize one could buy stakes in a general partner. Apparently some alt asset managers (GPs) allow investors to buy fractional ownerships in their own businesses. In return, investors collect a portion of management fees and carried-interest they generate.

- Sports league ownerships

- As expected, these are fractional ownerships in a professional sports team, likely through a large private equity fund

- Private credit

- Any lending that is done through non-bank lenders

- Energy

- Investments in energy related projects including traditional, renewables, transition to renewables, etc.

- Venture capital

- As the name suggests, investments in startups or early-stage ventures

- Real estate

- This is widely understood asset type that covers all kinds of RE investing: commercial, residential, multi-family, industrial, etc.

- Secondaries

- This is another category that many individual investors aren’t aware of. This investment is about taking over an existing stake in a private fund from a limited partner, in other words, an LP stake that exchanges hands.

I recommend that you pick a copy of the book if you want to go deeper into any of these asset classes. Or go search online.

As one might expect from the title of the book, the two co-authors make a case that investing in alternatives could lead to financial freedom. And that these investments are accessible to retail investors too.

Two key factors they cite in favor of alts: (1) alts have little or no correlation with traditional investments and (2) they are also less volatile. Therefore, when added to a traditional portfolio of stocks and bonds, alts will diversify a portfolio and serve as ballast. And if we pick good managers, alts could also be a source of outperformance.

Less correlation with common stocks is evident for some of the alts. But less volatility? I’m not sure if this is the case. Alts only give an appearance of low volatility because they are not marked to market on daily basis. David Swensen, the late endowment fund manager, known for introducing alt investments to the institutional world, said this in his book, Pioneering Portfolio Management:

If two otherwise identical companies differ only in the form of organization—one private, the other public—the infrequently valued private company appears much more stable than the frequently valued publicly traded company.

Who really has access? Alts would fit nicely in a long-term investor’s portfolio except for one key issue: access. Alternatives require active investing. Unlike common stocks, there is no passive index fund one could invest in. From David Swensen’s book:

Investors in alternative asset classes must pursue active management since market returns do not exist in the sense of an investable passive option.

Investing in Alts generally requires access to some private fund run by a hands-on manager. As the book also makes it clear in the beginning, these private funds are only accessible to an “accredited investor” (minimum $1 million net worth). Or a SEC “qualified purchaser” (minimum $5 million net worth). These are hefty requirements for many individual investors. Even being an accredited investor only opens the door to a selected few private funds. Many other style-specific funds are only accessible to qualified purchasers and require substantial upfront capital commitment.

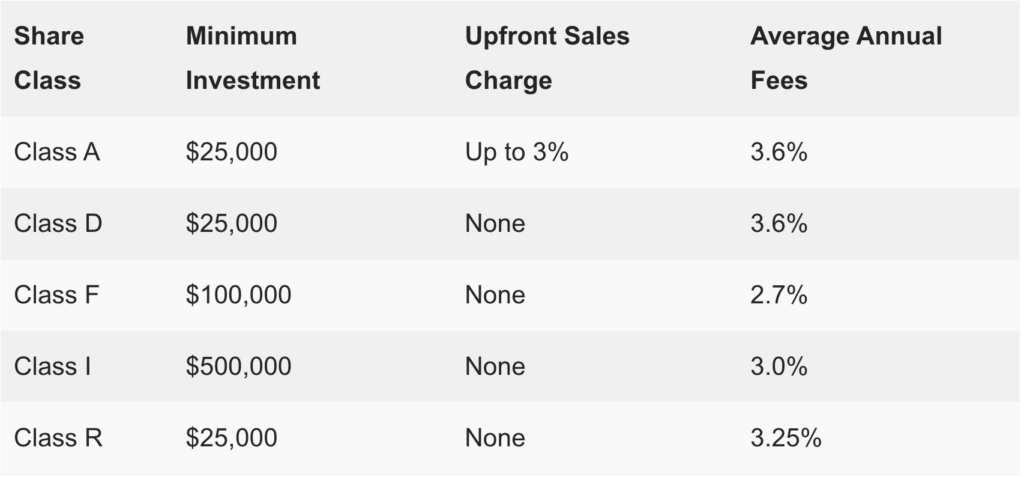

At what cost? If I invest with CAZ Strategic Investment Opportunities fund (the only fund available to accredited investors from the authors’ firm), I will pay 1.25% management fee plus various front-loaded sale charges (depending on the size of the principal). Total fee would amount to an average of 3.6%. See this table:

But there’re other hidden costs associated with such funds. These funds invest capital with other PE managers who generally charge 2-and-20 (2% annual fee plus 20% on any profits over and above some hurdle rate). Now granted they focus more on co-investments and secondaries (rather than direct investments in an effort to reduce total expenses) but still investors will pay much higher costs than expected from a fund that only invests in common stocks.

What credibility? If we are going to invest with a fund-of-funds that in turn allocates our capital to various other alt asset managers, we also need to consider trust and credibility concerns. Our performance will heavily depend on the capital allocation skills of the fund management team. How long has the team been together? How good is their long-term track record? You won’t find a lot of relevant data on their respective web sites since regulations limit public disclosure. Historical data is usually only available to prospective investors upon request.

Liquidity concerns? Investing in any non-traded fund brings some unique withdrawal challenges. This is true not just for private equity funds but also REITs and MLPs. (For instance, see my comments on BREIT in this post.) Here investors also have restrictions on how often they can exit a position (once a quarter) and how much can be withdrawn (less than 5% of fund’s assets).

An alternative? One other way to invest in alternative investments is by owning shares of publicly traded alt asset managers. Wouldn’t that be a simpler option for individual investors to implement? Rather than worry about high expenses, unproven track records, and cumbersome withdrawal rules, one could just invest through the stock market. I wonder why the book failed to mention that possibility.

Many large alt asset managers are publicly traded businesses. Majority of them have also converted from partnerships to C-corporations in recent years. Many run capital-light business models where they distribute all their earnings back to shareholders every quarter. We could just buy their shares in the open market to participate in their growth.

Buying shares of publicly traded alt asset managers is exactly like investing in GP stakes with all the same advantages that the book pitches. We get a stake in the manager’s investing strategies, broadly spread over numerous vintages of their private funds, and expanding scale as the firm grows its “assets under management”.

There are no liquidity concerns when we buy public businesses. We won’t need to hire a wealth manager or open an advisor-run account. No fees or charges for starting or exiting our positions either.

If you already have an on-going relationship with a wealth advisor (i.e. you’re paying him for his services) and you prefer your advisor to manage your portfolio, you’d be a good candidate for investing directly in a private fund like the book suggests. Perhaps you prefer a private fund because unlike publicly traded shares, it won’t distract you with daily quotes.

But you still need to be at minimum an accredited investor to qualify for investing directly. Even better, if you pass the muster as a SEC-qualified purchaser.

If you do decide to go this route, I should point out that CAZ is not the only fund manager you should consider. There are other good alternatives too, some with longer and more distinct investing history. Two that I recommend investors should look into are: JPMorgan Private Market fund and AMG Pantheon fund. Both have similar fee structure as CAZ Strategic Opp fund.

I am a believer in alternate investments. I’ve written about them in previous years. I like them in my portfolio that otherwise comprise of mostly stocks and some cash. I wrote about my hard assets and real estate related stocks here and here.

But I take a different approach for my alt investments than the one Tony Robbins promotes. I prefer a low-cost self-researched way to get into alts. I am a DIY investor who likes researching businesses.

Even though I meet the SEC definition for “qualified purchaser”, I am not interested in putting my capital in some private fund with scant prior record. I also don’t mind dealing with the volatility of daily price fluctuations of publicly traded stocks. It comes with the territory. I feel comfortable investing with managers whose audited performance records are public and span decades. I’m good at ignoring near-term volatility when I trust long-term vision of a business manager.

Today I am invested in two of the world’s largest alt asset managers. Both are publicly traded on NYSE. Both are broadly diverse in the type of strategies their sponsored private/public funds run. One is the largest manager of alt assets in the world, recently surpassing $1T AUM mark. The other is the largest Canada-based alt asset manager. They are Blackstone (BX) and Brookfield (BAM & its parent company BN) respectively.

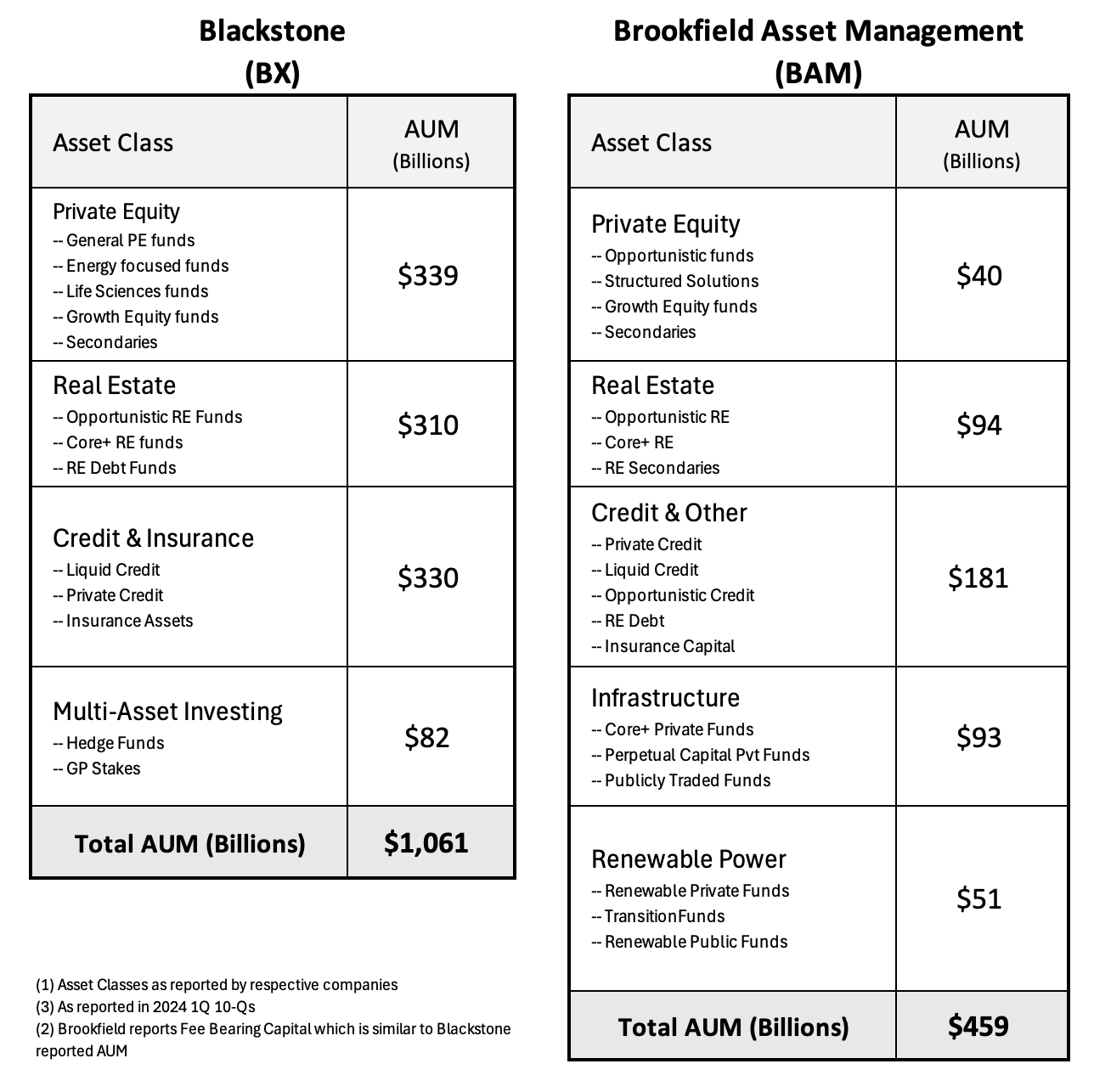

You can see in the below tables how well diversified they are in terms of investing strategies. Blackstone is highly regarded for its private equity and real estate funds. Brookfield is well-known for credit (with Howard Marks’ Oaktree under its wing), infrastructure, and energy funds.

I’ve written about both Blackstone and Brookfield several times on these pages, so I won’t rehash my investment theses. They are both excellent long-term oriented businesses, run by two very long tenured (20+ years) founder-CEOs. Read the following posts for more details: Why I am buying Blackstone, Brookfield passes my sniff test.

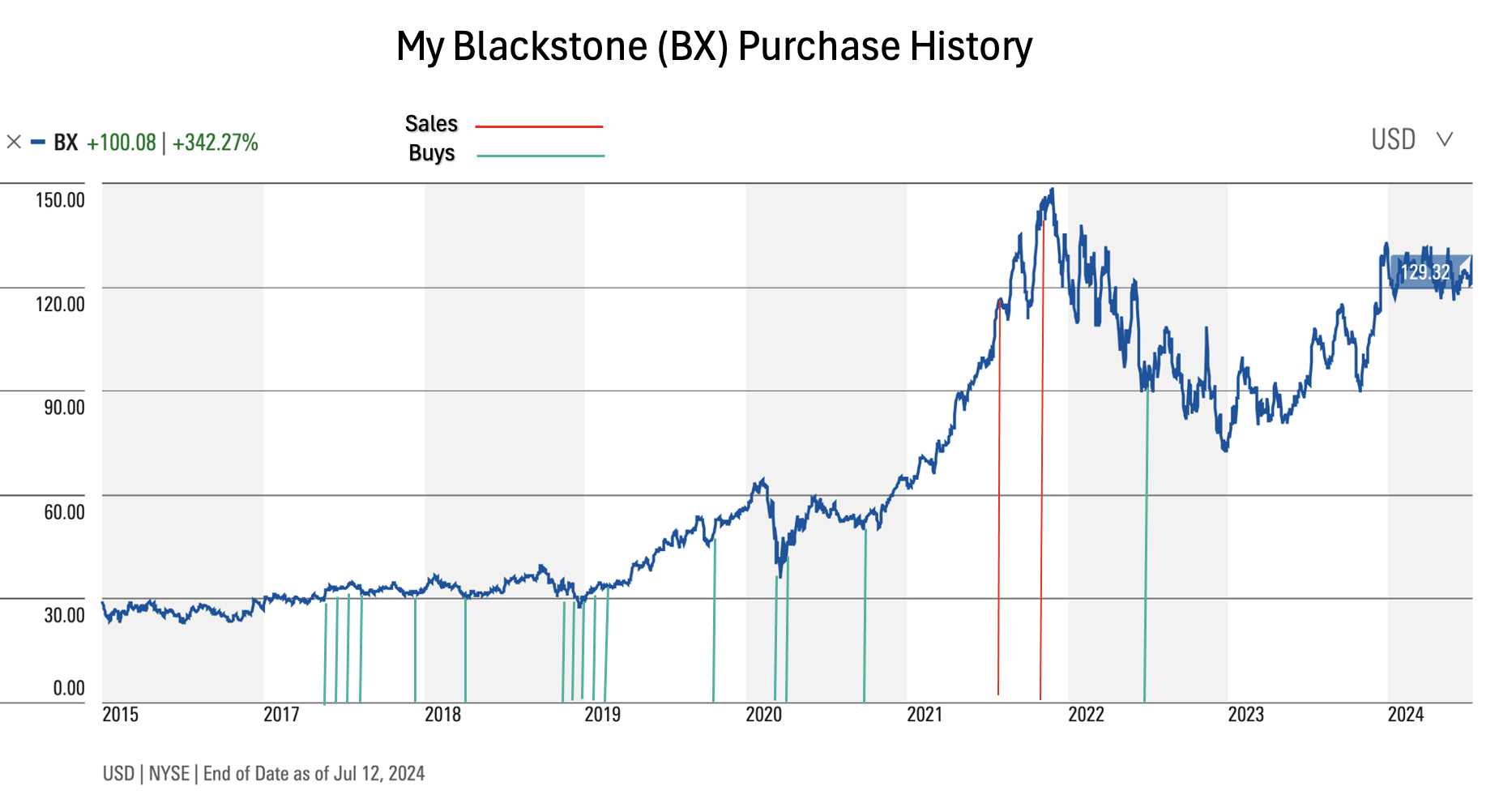

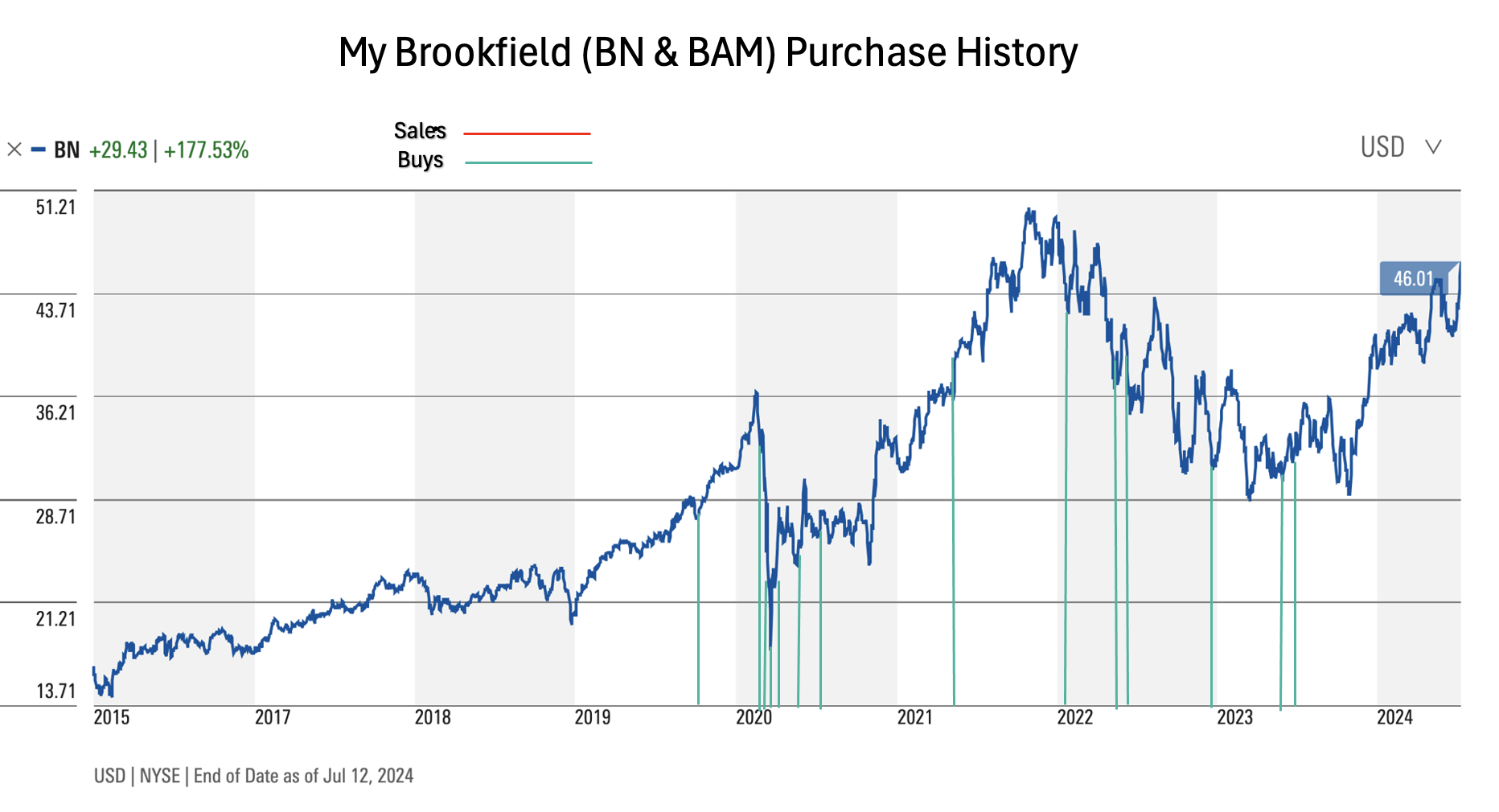

I own Blackstone shares since 2017. And Brookfield since 2019. Today both are in my top-20 positions.

I was introduced to Brookfield by Howard Marks when his firm, Oaktree, was acquired by Brookfield in 2019. I took advantage of the 2020 and the 2022 bear markets to aggressively build my Brookfield position.

Blackstone is an older position for me. From the time when it was a PTP (publicly traded partnership) and sent schedule K-1 forms every year. Today it is a C corporation and a member of the S&P 500 index. I got interested in Blackstone when I followed Tony James from the Costco board (since 1988) to his Blackstone employment (ex-COO, now retired).

Blackstone’s policy is to distribute 85% of its earnings to shareholders in form of dividends. Similarly, Brookfield BAM filings show it also intends to distribute 90% of its earnings back to shareholders. I feel confident that, ten years from now, I will still be a shareholder in these two businesses. My capital is in good hands.

Leave a Reply